Writer: Eric Bank

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

Owning one of the best credit cards for families seems like an intelligent response to these challenging times. Maybe you can’t do much about the world’s economic and political uncertainties, but you can ensure you get top card membership rewards and benefits on almost everything you purchase.

Families can consume mountains of food, require gas-guzzling chauffeuring, and turn travel into chaos. If that sounds like your clan, the credit cards in this review can save you money and perhaps make your activities a bit more fun.

Skip to the best cards for:

-

Navigate This Article:

Best Family Credit Card For Groceries

Shopping for a family, especially a large one, can be a nightmare. If your regular trip to the grocery store involves two shopping carts, you’ll love the Bank of America® Customized Cash Rewards credit card from Bank of America.

- $200 online cash rewards bonus after you make at least $1,000 in purchases in the first 90 days of account opening.

- Earn 6% cash back for the first year in the category of your choice. You’ll automatically earn 2% cash back at grocery stores and wholesale clubs, and unlimited 1% cash back on all other purchases. After the first year from account opening, you’ll earn 3% cash back on purchases in your choice category.

- Earn 6% and 2% cash back on the first $2,500 in combined purchases each quarter in the choice category, and at grocery stores and wholesale clubs, then earn unlimited 1% thereafter. After the 3% first-year bonus offer ends, you will earn 3% and 2% cash back on these purchases up to the quarterly maximum.

- No annual fee and cash rewards don’t expire as long as your account remains open.

- Select your card design option when you apply – the Customized Cash Rewards design, or the limited-time FIFA World Cup 2026™ design.

- 0% Intro APR for 15 billing cycles for purchases, and for any balance transfers made in the first 60 days. After the Intro APR offer ends, a Variable APR that’s currently 17.49% – 27.49% will apply. A 3% Intro balance transfer fee will apply for the first 60 days your account is open. After the Intro balance transfer fee offer ends, the fee for future balance transfers is 5%. Balance transfers may not be used to pay any account provided by Bank of America.

- This offer may not be available elsewhere if you leave this page. You can take advantage of this offer when you apply now.

Additional Disclosure: Bank of America is a CardRates advertiser.

This is far and away one of the best credit card for customized rewards and grocery store purchases. Its gas rewards are pretty good, too. With a $0 annual fee and lengthy intro 0% APR promotions on both purchases and balance transfers, you’d be hard-pressed to find a credit card friendlier than the Bank of America® Customized Cash Rewards credit card for you and your hungry brood.

Best Family Credit Card For Gas

The Discover it® Cash Back is a gas card, but only if you so choose. Earn 5% cash back in rotating categories up to the quarterly maximum when you activate. Common categories include gas stations, grocery stores, restaurants, and more.

- INTRO OFFER: Unlimited Cashback Match for all new cardmembers. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards. You could turn $150 cash back into $300.

- Earn 5% cash back on everyday purchases at different places you shop each quarter like grocery stores, restaurants, gas stations, and more, up to the quarterly maximum when you activate. Plus, earn unlimited 1% cash back on all other purchases.

- Redeem cash back for any amount. No annual fee.

- 0% intro APR on purchases and balance transfers for 15 months; 17.49% – 26.49% variable APR after that; balance transfer fee applies.

- Terms and conditions apply.

You can redeem your cash back for any amount at any time. Discover is also unique in that it offers to double all your earned cash back at the end of your very first year. Cardmembers also enjoy lengthy introductory periods on both purchases and balance transfers all with no annual fee. Keep in mind, the regular 17.49% - 26.49% Variable APR will apply at the close of the promotional periods.

Best Family Credit Card For Dining Out

Family visits to restaurants, even those that serve fast food, can put a dent in your budget. The Citi Strata Premier® Card pays generous rewards on dining out, takeout, and meal delivery to households with good to excellent credit.

- Earn 60,000 bonus ThankYou® Points after spending $4,000 in the first 3 months of account opening, redeemable for $600 in gift cards or travel rewards at thankyou.com.

- Earn 10 Points per $1 spent on Hotels, Car Rentals, and Attractions booked on CitiTravel.com.

- Earn 3 Points per $1 on Air Travel and Other Hotel Purchases, at Restaurants, Supermarkets, Gas and EV Charging Stations.

- Earn 1 Point per $1 spent on all other purchases

- $100 Annual Hotel Benefit: Once per calendar year, enjoy $100 off a single hotel stay of $500 or more (excluding taxes and fees) when booked through CitiTravel.com. Benefit applied instantly at time of booking.

- No expiration and no limit to the amount of points you can earn with this card

- No Foreign Transaction Fees on purchases

Additional Disclosure: Citi is a CardRates advertiser.

While the annual fee isn’t zero, you’ll easily make back the cost in rewards if you’re a frequent foodie, especially one that travels. Add in the lucrative signup bonus and travel perks and credits, and you’re likely to come out well ahead.

Best Family Credit Card For Everyday Spending

Everyday spending happens every day when you’re taking care of your family. The Citi Double Cash® Card provides 2% back on everything you buy without the worry of rotating categories, because you have enough to remember already.

- Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

- Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 17.49% – 27.49%, based on your creditworthiness.

- Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

- If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Additional Disclosure: Citi is a CardRates advertiser.

The card frequently offers a signup bonus and an intro 0% APR on balance transfers as well. The Citi Double Cash® Card provides family-friendly perks like access to the Citi ThankYou® Rewards program and zero liability for fraudulent purchases.

Best Family Credit Card For 0% Interest

Families frequently face big-ticket purchases, from 80-inch TVs to triple-capacity washing machines. Chase Slate Edge℠ gives new cardmembers a long introductory period of 0% APR on purchases (and balance transfers too).

- 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers, a variable APR thereafter. Balance transfers made within 120 days from account opening qualify for the introductory rate.

- $0 Annual Fee

- Get up to $600 of cell phone protection when you pay your monthly cell phone bill with your eligible Wells Fargo card (subject to a $25 deductible).

- Through My Wells Fargo Deals, you can have access to personalized deals from a variety of merchants. Activate your deals, then shop, dine, or enjoy an experience using an eligible Wells Fargo credit card.

- Zero liability protection plus Roadside Dispatch®

Additional Disclosure: The information related to this card has been collected by CardRates and has not been reviewed by the issuer of this product.

The card doesn’t dilute your rewards with an annual fee and offers 0% APR on balance transfers and purchases for a lengthy period. Moreover, you can also receive up to $600 in mobile device protection benefits if you use the card to pay your cell phone bill each month.

Best Family Credit Card For Travel

The Chase Sapphire Preferred® Card offers bonus points worth 1.25X more when you redeem them through Chase Travel. Just think — you could add an extra day to your four-day hotel stay when you pay with those bulked-up points.

- Earn 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening.

- Enjoy benefits such as 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases

- Earn up to $50 in statement credits each account anniversary year for hotel stays through Chase Travel℠

- 10% anniversary points boost – each account anniversary you’ll earn bonus points equal to 10% of your total purchases made the previous year.

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Collision Damage Waiver, Lost Luggage Insurance and more.

- Complimentary DashPass which unlocks $0 delivery fees & lower service fees for a min. of one year when you activate by 12/31/27. Plus, a $10 promo each month on non-restaurant orders.

- Member FDIC

Additional Disclosure: Non-Monetized. The information related to Chase Sapphire Preferred® Card was collected by CardRates and has not been reviewed or provided by the issuer of this product/card. Product details may vary. Please see issuer website for current information. CardRates does not receive commission for this product.

The Chase Sapphire Preferred® Card pays its highest rewards rate for hotel stays and other travel expenses booked through the Chase website. It also provides an annual hotel credit, trip cancellation and baggage delay insurance, and a 10% anniversary bonus point boost.

Best Family Credit Card For Amusement Parks

Family life can be a rollercoaster, especially when you spend a day or two at an amusement park. The Capital One Savor Cash Rewards Credit Card can smooth out the bumps with bonus rewards on entertainment and dining expenses, including amusement and theme park purchases.

- For a limited time, earn a one-time $250 cash bonus once you spend $500 on purchases within the first 3 months from account opening

- $0 annual fee and no foreign transaction fees

- Earn unlimited 3% cash back at grocery stores (excluding superstores like Walmart® and Target®), on dining, entertainment and popular streaming services, plus 1% on all other purchases

- Earn 8% cash back on Capital One Entertainment purchases

- Earn unlimited 5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

- No rotating categories or sign-ups needed to earn cash rewards; plus cash back won’t expire for the life of the account and there’s no limit to how much you can earn

- 0% intro APR on purchases and balance transfers for 12 months; 18.49% – 28.49% variable APR after that; balance transfer fee applies

- Top rated mobile app

The card’s customary signup bonus and 0% intro APR can make your experience more affordable. You also get 24-hour travel assistance, complimentary concierge services, and travel accident insurance. You can redeem your rewards for a statement credit, gift card, or in several other ways.

Best Premium Family Credit Card

The Chase Sapphire Reserve® is our favorite premium credit card for families, and one of the best credit card offers on the planet. This rewards card provides emergency evacuation services should a family member experience an injury or illness on a trip abroad, among several other industry-leading travel insurance benefits.

- Earn 125,000 bonus points after you spend $6,000 on purchases in the first 3 months from account opening.

- Get more than $2,700 in annual value with Sapphire Reserve.

- Earn 8x points on all purchases through Chase Travel℠, including The Edit℠ and 4x points on flights and hotels booked direct. Plus, earn 3x points on dining worldwide & 1x points on all other purchases

- $300 annual travel credit as reimbursement for travel purchases charged to your card each account anniversary year.

- Access over 1,300 airport lounges worldwide with a complimentary Priority Pass™ Select membership, plus every Chase Sapphire Lounge® by The Club with two guests. Plus, up to $120 towards Global Entry, NEXUS, or TSA PreCheck® every 4 years

- Get up to $150 in statement credits every six months for a maximum of $300 annually for dining at restaurants that are part of Sapphire Reserve Exclusive Tables.

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Coverage, Lost Luggage Insurance, no foreign transaction fees, and more.

- Get complimentary Apple TV+, the exclusive streaming home of Apple Originals. Plus Apple Music — all the music you love, across all your devices. Subscriptions run through 6/22/27 — a value of $250 annually

- Member FDIC

Additional Disclosure: Non-Monetized. The information related to Chase Sapphire Reserve® was collected by CardRates and has not been reviewed or provided by the issuer of this product/card. Product details may vary. Please see issuer website for current information. CardRates does not receive commission for this product.

The card is chockablock with perks that repay the steep annual fee. If you like to travel, the free airport lounge access for you and your family can justify the yearly charge. You also receive several annual and monthly credits, such as reimbursement for TSA Precheck and Global Entry fees.

Best Credit Card For Families With Poor Credit

Even though the Capital One Quicksilver Secured Cash Rewards Credit Card is for applicants with no or poor credit history, it will still pay you cash back on every purchase you make. Pay your balance in full each month to reap the rewards and see upward progress in your credit score over time.

- No annual or hidden fees, and you can earn unlimited 1.5% cash back on every purchase, every day. See if you’re approved in seconds

- Put down a refundable $200 security deposit to get at least a $200 initial credit line

- Building your credit? Using a card like this responsibly could help

- Enjoy peace of mind with $0 Fraud Liability so that you won’t be responsible for unauthorized charges

- You could earn back your security deposit as a statement credit when you use your card responsibly, like making payments on time

- Be automatically considered for a higher credit line in as little as 6 months with no additional deposit needed

- Earn unlimited 5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

- Monitor your credit score with CreditWise from Capital One. It’s free for everyone

- Top rated mobile app

You’ll need to a pay a security deposit to get this card, but the full amount is refundable as soon as six months when you consistently pay your monthly bill on time. There’s no annual fee or monthly service fee that many unsecured cards for bad credit charge, making this a much cheaper option for building credit in the long run.

How Do I Choose The Best Credit Card For My Family?

Households have widely differing needs that rely on various factors. You want to own credit cards with the rewards and benefits that best suit your family’s spending and, perhaps, travel preferences.

One-size-fits-all definitely doesn’t apply to choosing the best card for your family. A married couple may be satisfied with a general-purpose rewards card that offers the same amount of cash back on all purchases. But add children, and suddenly you’re spending money on many new products and services.

Shopping for groceries and clothing becomes more extensive and more expensive. Chauffeur duties require more fill-ups at the pump. Travel, entertainment, and dining all become more elaborate and costly.

Income is another important factor influencing a family’s choice of cards. Folks living on a tight budget don’t typically splurge on premium credit cards with three-digit annual fees. On the other hand, affluent families may be willing to pay for expensive credit cards loaded with perks such as airport lounge access.

Life events, such as getting married, purchasing a house, and childbirth, often involve significant buying sprees for big-ticket items. A new credit card with generous introductory promotions and a healthy credit limit comes in handy when the bills for new appliances and furniture mount quickly. A large signup bonus and an intro 0% APR will reduce the overall cost of major purchases.

Your credit card choices are virtually unlimited if you have good or excellent credit. Not so if you have fair or bad credit. If you fall into the latter category, obtaining a credit card that pays rewards and doesn’t impose high fees will be a victory.

Families with poor or no credit may do best with secured credit cards. They are easy to get if you can afford the refundable deposit. As an extra benefit, secured cards are more likely to offer perks and cost less than unsecured cards for subprime consumers.

Sending children off to college is an opportunity for them to own credit cards, perhaps for the first time. Student credit cards may offer the best deals in the industry, as they don’t require any credit history for approval and often pay rewards and credits. Students under 21 years of age must demonstrate income or have a cosigner to qualify for a credit card.

Families that like to take trips may want to own one or more travel rewards credit cards. These pay rewards in miles and points, especially for travel-related purchases — flights, hotel stays, rental cars, cruises, etc.

The bonus point balances on several premium travel rewards cards gain extra value when you redeem them through the issuer’s travel portal, i.e. Chase Ultimate Rewards, Capital One Travel, etc.

Families can choose to own general-purpose travel cards that save money on all flights, co-branded cards for specific brands, or a mix of both. Some travel cards offer multiple credits, such as for Global Entry or TSA Precheck reimbursements.

Once you assess your family’s overall credit needs, you’ll have an idea of how to narrow your choices based on several credit card attributes, including:

- Credit requirements: These depend on your FICO score and credit report.

- Signup bonuses: Check the amount of spending required during the introductory period and the size of the bonus.

- Introductory 0% interest rate: If offered, see how long it lasts and if it also applies to balance transfers.

- Purchase APR: This may be a single percentage or a range, no higher than 36%. The card may have different balance transfer and cash advance APRs. Some cards impose a penalty APR if you miss a payment.

- Fees: These include the annual fee plus charges for late payments, cash advances, balance transfers, additional cards, etc. Many cards also charge foreign transaction fees. Cards for subprime consumers may tack on signup and monthly maintenance fees.

- Grace period: This is the interest-free period between the end of a billing cycle and the payment due date. If present, it must last at least 21 days. Avoid cards that do not have a grace period.

- Rewards: These may take the form of bonus points, cash back, or miles. Some rewards cards pay a flat, single-tier reward on all purchases. Others provide multitiered rewards based on merchant type (e.g., airlines, hotels, restaurants, etc.). Cards may offer quarterly rotating merchant categories that you must activate to receive bonus rewards. Issuers may place quarterly or annual limits on rewards.

- Benefits: Cards may offer broad categories of benefits, such as those related to travel, consumer protections, and credit monitoring.

- Credit line: Your credit line is the amount you can charge with your credit card. It can range from $200 to more than $100,000. For virtually all secured cards, the credit line equals the security deposit.

- Balance transfer availability: Many credit cards let you consolidate the unpaid balances from other cards. Seek out balance transfer promotions featuring an introductory 0% APR for new card members.

If you start with a secured credit card, you’ll want to know how long it will take to graduate to an unsecured one.

Can I Get a Credit Card For a Family Member?

Virtually all credit cards allow cardmembers to add authorized users to their accounts. Authorized users can be added to a credit card account by the primary cardholder and charge purchases with their card, but they are not legally responsible for making payments.

Married cardmembers routinely make their spouses authorized users. You can also add children, although some cards set minimum age limits:

- American Express: 13

- Bank of America: None

- Barclays: 13

- Capital One: None

- Chase: None

- Citi: None

- Discover: 15

- US Bank: 16

- Wells Fargo: None

Some issuers charge a one-time fee for each additional card.

There are several good reasons to make your children authorized users of your credit card:

- Establishing a credit history: By starting early, your child can build a good credit score and a solid credit report that facilitate lower interest rates on loans and credit cards, often without you needing to be a cosigner.

- Obtaining protection: Credit cards provide $0 liability protection when lost or stolen. Some also offer purchase protection against theft or damage to recently bought items.

- Earning rewards: Cardowners collect the rewards earned by their children, often as a statement credit or gift card. This teaches kids a valuable lesson.

- Handling emergencies: A credit card can reassure minors that they won’t suddenly find themselves stranded without money to pay for a meal or a tank of gas.

- Learning about personal finance: Parents can teach their children how to manage credit, avoid interest expenses, and reduce credit utilization. A few issuers let you set lower credit limits for authorized users and monitor their spending in real time.

As mentioned, a parent (or another responsible adult) must cosign a student credit card application for children between ages 18 and 21 who don’t earn an income.

How Many Credit Cards Does My Family Need?

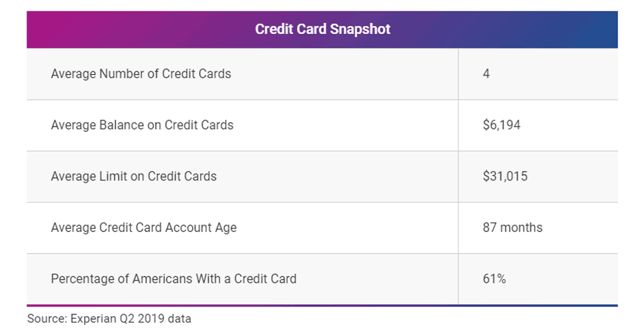

The following data collected from Experian can help clarify how much credit your family may need:

If your family owns four credit cards with a total credit limit of around $31,000, it’s about average for the US, where 61% of consumers have at least one credit card. These numbers exclude student loans, mortgages, and other types of debt.

Your family decides how many credit cards to own, and some think the correct number is zero. That’s certainly one way to avoid debt, but it is not without cost. If you don’t own a credit card, it becomes harder to finance purchases of big-ticket items, which can negatively impact your lifestyle.

Ask yourself whether your family can purchase whatever it wants with your current credit cards and whether your credit score would improve if you altered the number of cards you own. The answer to the first question depends on your spending needs versus your credit limit, and whether you have to depend too much on your debit card.

The second question pertains to your credit utilization ratio (i.e., credit spent divided by total credit available), which ideally should be below 30%, as higher ratios can damage your credit score. If your CUR is too high, you may benefit from additional credit cards to increase your available limit, as long as you don’t use them to go on a shopping spree — consider using your debit card instead.

Here is an example of CUR calculated on three separate card accounts:

You should reassess your use of credit if you find it hard to pay your monthly credit card bills. But don’t cancel old credit card accounts as this may hurt your credit score.

How Do I Protect My Family From Credit Card Fraud?

Credit cards routinely provide $0 fraud liability protection against card loss or theft. Naturally, you want your family to use their credit cards safely, such as by:

- Observing proper password security, including using strong unique passwords you don’t use elsewhere, and changing them every six months.

- Using two-factor authentication whenever you make an online purchase. This requires the merchant to send you a secret code (by email or phone) to enter before you can use the card.

- Not sharing your credit card number on public networks. When using public wifi, you can defeat hackers by configuring your computer with a Virtual Private Network (VPN).

In addition, don’t click on email links, even if you recognize the sender. Phished emails lead to identity theft. You can avoid this by contacting the sender independently of the email.

It’s a good practice to sit down with family members to discuss proper procedures for using your credit cards safely.

Your Family Deserves Great Credit Cards

Your loved ones deserve nothing but the best. Our article about the best credit cards for families is one way to ensure they get it. Whether you need just a single card or a dozen, you will get the most value by choosing cards that receive top ratings.

Our ratings are independent and unbiased, so you can count on them to give you the facts without any nonsense.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/06/Can-I-Use-My-Credit-Card-Before-Closing-on-a-Home.jpg?width=158&height=120&fit=crop "Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=\" (\" after=\")\"]")

![List of Subprime Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/10/list.jpg?width=158&height=120&fit=crop "List of Subprime Credit Cards[updated_month_year before=\" (\" after=\")\"]")

![[updated_month_year after=" "]Cash Advance Limits by Issuer[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2020/12/shutterstock_2980733.jpg?width=158&height=120&fit=crop "[updated_month_year after=\" \"]Cash Advance Limits by Issuer[updated_month_year before=\" (\" after=\")\"]")

![5 High Credit Line Credit Cards for Fair Credit[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2021/07/High-Credit-Line-Credit-Cards-For-Fair-Credit.jpg?width=158&height=120&fit=crop "5 High Credit Line Credit Cards for Fair Credit[updated_month_year before=\" (\" after=\")\"]")

![7 Best First Credit Cards, No Credit Needed[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/07/firstcard.png?width=158&height=120&fit=crop "7 Best First Credit Cards, No Credit Needed[updated_month_year before=\" (\" after=\")\"]")

![7 Best High-Limit Credit Cards for Fair Credit[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/11/fair-credit-limits-art.jpg?width=158&height=120&fit=crop "7 Best High-Limit Credit Cards for Fair Credit[updated_month_year before=\" (\" after=\")\"]")

![8 Best Credit Cards for High Credit Scores[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2019/10/Best-Credit-Cards-for-High-Credit-Scores-Feat.jpg?width=158&height=120&fit=crop "8 Best Credit Cards for High Credit Scores[updated_month_year before=\" (\" after=\")\"]")

![9 Best Credit Cards by Credit Score[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2020/11/shutterstock_402532915.jpg?width=158&height=120&fit=crop "9 Best Credit Cards by Credit Score[updated_month_year before=\" (\" after=\")\"]")