Eric Bank is an M.B.A. who has covered financial and business topics since 1985, appearing regularly on Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences, particularly in the world of personal finance. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.

Lillian Guevara-Castro brings more than 30 years of editing and journalism experience to the CardRates team. She has worked at The Atlanta Journal and Constitution, Gwinnett Daily News, Gainesville Sun, and The New York Times, where she covered demographics, consumer issues, and the business and financial sectors. Lillian has a degree in journalism and communications from Georgia State University and brings her fact-checking expertise to ensure Digital Brands content is accurate and engaging.

Ashley Fricker has more than a decade of experience as a finance contributor and editor, and has specialized in the credit card industry since 2015. Her credit card commentary is featured on national media outlets that include CNBC, MarketWatch, Investopedia, and Reader's Digest, among many others. She has worked closely with the world’s largest banks and financial institutions, up-and-coming fintech companies, and press and news outlets to curate comprehensive content and media. Ashley holds a bachelor's degree in multimedia journalism from Florida Atlantic University.

Below are our picks for 2026's best credit cards featuring instant approval. Note that most issuers of cards for good credit, fair credit, and poor credit do not offer instant approval. Our reviews follow strict editorial guidelines and are updated regularly.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

The secured Self Visa® Credit Card* requires no credit check or minimum score.

Reports to all 3 major credit bureaus to establish and build credit, with free access to your credit score.

Secure your credit line with a refundable security deposit as low as $100.**

Deposits are returned upon account closure after settling outstanding balances.

*The secured Self Visa® Credit Card is issued by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC.

**Qualification for the secured Self Visa® Credit Card is based on meeting eligibility requirements, including income and expense requirements and establishment of security interest. Criteria subject to change.

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APRVariable APR of 27.49%

Annual Fee$0 annual fee for the first year only, $25 annual fee thereafter

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

^^1% Cash Back is earned on payments to your Credit Card. Up To 10% Cash Back is earned on qualifying purchases at select participating merchants. Offer percentages vary by merchant and are subject to change. See Total Card Visa Rewards Programs Terms & Conditions for details

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Review Breakdown

Unfortunately the options for "instant approval" credit cards are very limited, as the vast majority of issuers of cards for good credit, fair credit, and poor credit offer quick (but not instant) approval. We encourage you to visit those links to find better offers for your situation. Below is a summary of the limited options for truly instant approval.

Here are 2026's best instant approval credit cards:

Welcome to our compilation of answers to your most burning questions about the best instant approval credit cards. As it happens, most credit cards offer an instant decision, or at least instant preapproval.

A little knowledge can greatly improve your chances of approval. Gain a tactical advantage by spending the next few minutes learning how to obtain a credit card with minimal fuss.

1. What is an Instant Approval Credit Card?

The concept of “approval in an instant” needs a little context. On its face, instant credit card approval means a decision in seconds, or perhaps a few minutes. But many applicants would settle for a same-day decision if it were positive. A speedy decision is not such a virtue if it’s a “no.”

Make no mistake — credit card issuerswant to approve you and to do so quickly. Issuers know that a delayed decision gives you the opportunity to apply for another card that may be more forthcoming with an approval. This is why you’ll see many credit card ads promising instant prequalification, which is a savvy move by issuers.

If you prequalify for a card, issuers have at least one hook into you that can reduce your desire to apply elsewhere. That’s great if you eventually are approved — and it costs the card issuer nothing. The bottom line is that it’s unusual for issuers to delay feedback on your application, making “instant approval” a feature that perhaps is worth less than advertised.

2. How Does an Instant Approval Credit Card Work?

There is nothing special about how an instant approval credit card operates. If you have good or excellent credit, you expect instant approval — the issuer should be grateful you’re giving it your business, right?

However, we’d venture that many consumers want instant approval because they are worried about a low credit score or scant credit history. If you have a bad score, a fast decision avoids an anxious waiting period. In fact, some folks may prefer fast disapproval than a dragged-out process that may finally result in approval.

That’s why it’s essential to understand how instant approval credit cards work for applicants with poor credit. These cards, often catering to the subprime community, typically have extra fees, low credit limits, limited perks, and high interest rates. In fact, the ability to approve applications swiftly might be their greatest advantage.

Given the constraints that accompany the bad-credit slice of the instant approval universe, it’s really important that these cardholders scrupulously follow the rules to receive approval on a credit card application. That means always paying on time, paying at least the minimum required amount, and never exceeding the credit limit. Good behavior will translate into minimal extra fees and, eventually, a higher credit score.

Naturally, responsible use of credit is important to all cardholders. The difference is that cardmembers with poor credit have much less wiggle room, both in terms of how penalty fees impact their monthly budgets and how a drop in an already-low credit score will further complicate their ability to borrow or get additional credit.

There’s another group to which instant approval is of paramount importance. We’re talking about shoppers who find themselves staring at a fleeting deal without sufficient credit to take advantage of it. As we’ll discuss below, instant approval cards that also provide same-day use can provide a shopping victory that will be savored for years to come.

Finally, let’s mention those consumers who need a small emergency loan despite having bad credit. They represent an intersection of those having poor credit and those who want same-day credit card use. For these folks, the ability to get a fast cash advance can be a real problem-solver, and certainly beats alternatives like payday or pawnshop loans.

3. How Do I Get an Instant Approval Credit Card?

Most cards offer instant preapproval, which is almost as good as instant approval. We say almost as good because preapproval doesn’t guarantee final approval — it merely puts the odds in your favor.

To get instant preapproval, first decide which credit card you want. To that end, we regularly publish reviews of the best instant approval cards. Consider cards that fit your needs in terms of credit requirements, rewards and benefits, introductory 0% APR promotions for balance transfers, and specialized challenges faced by students and businesses.

Having chosen the card you want, visit the issuer’s website by clicking its name or the Apply Now button above and complete the online prequalification form. This will require some basic information about yourself, your income, and your expenses. After submitting the form, the issuer will immediately perform a soft inquiry on your credit report.

Soft inquiries provide issuers with only partial information, but it’s usually enough to render a decision regarding preapproval. You benefit from a soft inquiry because it doesn’t hurt your credit score. If you are preapproved and ask for final approval, the issuer will (with certain exceptions) do a hard pull of your credit report before rendering its final decision.

Hard inquiries provide issuers with your complete credit history. Unfortunately, they may lower your credit score by five to 10 points for up to a year. That’s why the preapproval step is important — after all, there’s no reason to hurt your own credit score if you’re not going to get past the preapproval stage.

If you are approved, expect your card to arrive in about a week to 10 days. Some issuers may offer expedited shipping with or without a fee. For example, Discover delivers its credit cards using USPS Priority Mail at no extra cost. That cuts the delivery time to three to five days and also provides you with a tracking number so you can monitor the card’s location.

When you get the card, an attached sticker will direct you to a phone number or website to confirm receipt and activate the card. After doing so, you can remove the sticker and begin using the card.

If the card has a signature strip, affix your John Hancock proudly. Store the accompanying disclosure booklet someplace safe, as it will be helpful when you have questions about the card’s fees or benefits.

See FAQ #12 for information about cards you can start using even before they arrive in your mailbox.

4. Which Credit Cards Approve Applicants Immediately?

In today’s online environment, just about all cards offer immediate approval. The better question is which instant-approval cards are best for various groups of consumers. We’ve researched that question and the following are our top recommendations:

Bad credit: Capital One Platinum Secured Credit Card is easy to get because you deposit cash collateral to secure your credit line. You can use it to build credit because it reports your activity to each major credit bureau. This secured credit card charges no annual fee and may increase your credit limit over time with no additional security deposit.

Fair credit: Capital One Platinum Credit Card has no annual fee, supports contactless checkout, and lets you pick the monthly due date that works best for you. You also get fraud coverage and automatic consideration of a higher credit limit.

Cash back: Chase Freedom Unlimited® is our favorite instant approval cash back card, offering regular and bonus reward tiers, a signup bonus, an introductory 0% APR on purchases, and no annual fee. There’s no minimum redemption amount and your rewards don’t expire while the account remains open.

Air miles: Capital One Venture Rewards Credit Card offers a generous signup bonus and a flat rewards rate on all eligible purchases. You also get a reimbursement credit for Global Entry or TSA Pre✔® fees, mileage transfer to more than 10 loyalty programs, and no foreign transaction fee.

Balance transfer:Citi Simplicity® Card provides an introductory 0% APR on purchases and balance transfers while charging no late fee, no annual fee, and no penalty rate. It offers $0 liability protection and identity theft solutions, as well as your choice of payment due date.

Student: Capital One Quicksilver Student Cash Rewards Credit Card lets you earn a flat cash back rate on all eligible purchases and a small spend bonus. There are no annual or foreign transaction fees. Use the card to build your credit, and with responsible use, a higher credit limit.

Business:Ink Business Preferred® Credit Card offers tiered reward points and a substantial signup bonus. Points are worth more when redeemed for travel through Chase Ultimate Rewards. The card has no foreign transaction fees.

All these cards offer instant approval and receive our top ratings.

5. What is the Easiest Credit Card to Get Approved For?

Secured cards are the easiest to get and our top pick is the Capital One Platinum Secured Credit Card. It doesn’t require a minimum credit score because your deposit secures the card against missed payments and over-limit spending.

The initial credit line is $200, but you may be able to deposit less to secure the card. You can increase the initial credit limit by depositing additional money before opening the account.

Student credit cards are also easy to get (if you are a student), and, as noted earlier, our favorite is the Capital One Quicksilver Student Cash Rewards Credit Card. However, close behind in our ratings is the Bank of America® Customized Cash Rewards credit card for Students. It offers tiered cash back rewards, a signup bonus, and an introductory 0% APR on purchases and balance transfers.

6. Can I Get a Credit Card Same Day?

We’ve searched high and low but can’t find an issuer that can put a card in your hand on the same day your credit card application is approved. Some banks can give you an instant card, but it will be a debit card linked to a checking account, not a credit card.

Several cards do offer same-day usage for card not present (CNP) transactions. These cards are available from Capital One, American Express, Chase, Citi, and Barclays. See FAQ #12 for more information.

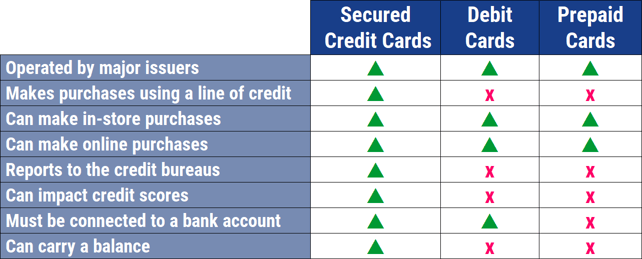

7. What is the Difference between a Secured and Unsecured Credit Card?

Most credit cards are unsecured, meaning they grant you credit on the strength of your creditworthiness. The amount and cost of credit are tied to your credit score although certain cards, such as ones for students or consumers with very bad credit, may waive a credit check.

Secured cards are a different kettle of fish. To obtain a secured card, you must deposit cash into a special locked account provided by the issuing bank. The refundable deposit collateralizes some or all of your initial credit line.

For example, a secured card may offer you a $200 credit limit but require you to deposit $200 into the account. Uniquely, the Capital One Platinum Secured Credit Card may require as little as $49 to secure the standard initial credit line of $200. You can increase the limit to up to $1,000 by depositing additional funds before activating the account.

Some secured cards may allow credit limits up to around $5,000. If you consistently pay your monthly bill on time, some issuers might increase your credit limit without requiring additional deposits. Eventually, the issuer may even refund your deposit and transition you to an unsecured card.

Secured cards look and, at purchase time, operate just as unsecured cards do, so the cashier at the checkout register won’t be any the wiser. You can use them for online purchases just as you would an unsecured card.

Secured cards have some other differences. Because the credit line is collateralized, these cards may offer a relatively low interest rate. Also, if your payment is late or you exceed the credit limit, the issuer will, on the first occurrence, take the shortfall from your security account and adjust your credit line. Repeated infractions may prompt the issuer to close the account.

Secured cards can easily receive instant approval. Ironically, they have a built-in delay — your deposit must arrive and clear before the issuer will send out the card. You can minimize this delay by opening the credit card at a bank or credit union branch where you already have a checking account. If the card is from a different issuer, you can cut the delay by arranging an electronic funds transfer from your bank account to the issuer’s security account.

A secured card is a good way to establish or rebuild your credit. Issuers of these cards routinely send your payment activity to each major credit bureau. It’s up to you to pay your bills on time and control your credit balance to benefit from transaction reporting.

Consumers who have a long history of paying their bills are likely to continue to pay their bills. If you have your sights set on a prime rewards credit card, you'll want at least six months (but preferably a year or more) of positive payment history.

Prepaid cards are similar to debit cards but don’t require you to have a bank account. They allow you to spend the money you load onto the card instead of whipping out cash or a check. There is no credit limit because there is no credit — just load the amount of money you want.

Groceries, pharmacies, box stores, and other retailers sell prepaid cards. You can load (and reload) prepaid cards at retail locations, online, over the phone, and even at some banks and credit unions. You can add money with cash, a check or money order, and direct deposits.

Our favorite prepaid card is the PayPal Prepaid Mastercard®. You can fund it from your PayPal account and earn cash back on purchases you make with the card. Because it’s a Mastercard, it’s accepted everywhere Mastercard is accepted. Visa prepaid cards are also available.

There are a couple of knocks against prepaid cards despite their instant approval. They don’t establish or build credit. Moreover, they are often saddled with many fees that reduce your card balance. They may charge fees for each purchase, reload, deposit, withdrawal, or by the month, among other possible fees.

9. Are There Instant Approval Cards for Poor Credit?

Poor credit should not keep you from owning an instant approval credit card. In fact, most cards aimed at folks with low credit scores (below 580 on the FICO scale) offer instant preapproval, which lets you know whether you qualify for a card without hurting your credit score. Keep in mind that preapproval doesn’t guarantee final approval.

If you truly want instant approval without the preapproval step, go for a secured card. As is true for all secured cards, your cash deposit collateralizes the card’s credit limit, making your bad credit irrelevant to the issuer’s approval.

You have some options if you want an unsecured instant-approval credit card despite a low credit score. Our top pick in this space is the Surge® Platinum Mastercard®, which welcomes applications from all consumers. Like most of its competitors, this card offers instant prequalification, comes with fees, and reports your monthly activity to the three major credit bureaus.

Another highly ranked instant approval card for bad credit is the Indigo® Unsecured Mastercard®. This card is geared toward consumers with imperfect credit histories, including prior bankruptcies. The card provides fast prequalification, mobile-friendly access, and fraud protectionif your card is lost or stolen.

10. Which Business Credit Cards Offer Instant Approval?

Business owners looking for an instant approval card should compare the rewards offered by a competing business credit card or two. Some benefits, such as free cards for employees and $0 liability protection, are common. Our three top picks are:

Ink Business Preferred® Credit Card: You earn tiered rewards in the form of points, and those points are worth 25% more when redeemed for travel through Chase Ultimate Rewards. The card offers a sizable signup bonus, no foreign transaction fees, and protections for travel, purchases, and cell phones.

Ink Business Cash® Credit Card: A tiered cash back business credit card with a modest signup bonus and an introductory 0% APR promotion for purchases. The card charges no annual fees while providing travel and emergency assistance services, extended warranty protection, and auto rental collision damage waiver.

Business Gold Card: This card lets you pick the two eligible purchase categories (for example, gas purchase and flight tickets) that will earn bonus points up to an annual limit in combined purchases. Points are worth 25% more when you book a flight with American Express Travel. The card offers a signup bonus, provides useful expense management tools, and has a moderately high annual fee.

Business credit cards allow you to collect rewards on the employee cards you hand out. They also can save you money on business-related purchases such as office supplies, business meals, and travel for work.

11. Do Store Cards Offer Instant Approval?

Hundreds of store cards are available that offer instant approval. That’s not surprising because many retail stores offer their own credit or charge cards to shoppers on the checkout line, where instant approval is a must. But online stores also offer instant approval cards and for pretty much the same reason — to grab consumers as they check out.

Most store cards are limited to purchases at the issuing store and perhaps some retail partners. Some popular store credit card brands with quick approval include:

Amazon.com Store Card: This card is handy for shopping on the Amazon.com website. It charges no annual fee, but it does carry a high APR, making it relatively expensive to carry a balance over multiple months. The Amazon Store Card may offer special financing deals when your order exceeds a specified minimum.

Target REDcard: You can use this card at Target stores and online at Target.com to save 5% on purchases. Like most store cards, it charges no annual fee and has a relatively high APR. The card caters to consumers with all types of credit, including FICO scores as low as 580.

Costco Anywhere Visa® Card by Citi: You must be a Costco member to get this card. The APR is lower than some other store cards, and you earn tiered cash back on Costco purchases. You get extended warranty protection and no-fee foreign transactions.

Store cards are more versatile when you can use them beyond the confines of the issuing retailer. Look for ones that offer good rewards, charge no annual fee, and are issued at stores that you would shop at even without the card.

12. Can I Use a Credit Card Before it Arrives?

If waiting overnight for your expedited credit card seems like an eternity, know that some credit cards can be used immediately after approval. Many of these cards provide an instant card number or virtual credit card number good for either one use or until your physical card arrives. The problem, however, is that not every issuer offers this feature, and it’s even less common with subprime card issuers.

Selected cards from American Express provide instant use. You must apply for these cards online and American Express must be able to instantly verify your identity. For example, the Blue Cash Preferred® Card offers instant use after approval.

Co-branded United Airlines/Chase cards, such as the United ClubSM Infinite Card, can be immediately used via your MileagePlus account to pay for United purchases. All other purchases require a physical card. Other Chase co-branded cards offer immediate credit through the Chase partner, including Marriott, British Airways, Southwest Airlines, Amazon, and Disney.

Several co-branded cards from Barclays, like the Uber Visa Card, offer instant credit for purchases from the card partner.

13. How Long Does it Take for a Credit Card to be Mailed?

Almost every major credit card company has large, efficient operations that may be able to print and dispatch a new card on the same or next day. Smaller issuers may take longer. The real question is how long before you can get your hands on the new card.

As noted earlier, Discover can put a card in your hand in three to five days thanks to expedited shipping. At least, that was true in previous years — turmoil at the U.S. Post Office may stretch out the delivery time.

Chase will, upon request, send out a card on the same day as approval with free expedited shipping. The card can arrive as quickly as overnight. You can request expedited shipping by calling its customer service number at 1-800-432-3117.

Capital One may expedite shipping if you ask, but there are no guarantees. There’s a similar policy at Bank of America. Some premium cards from American Express, such as Platinum and Delta-branded cards, are automatically expedited and may arrive in as few as two days.

14. How Will an Instant Approval Card Affect My FICO Score?

Instant approval cards have no greater impact on your FICO score than do slowpoke cards — the impact is just, well, faster. When you get a new card, your FICO score may go up or down, depending on your financial circumstances. Here’s how a new card factors into your FICO score:

Credit utilization ratio (CUR): Your CUR, which accounts for 30% of your FICO score, is the amount of credit you’ve used divided by your total credit limits. A new card adds the new credit limit to the denominator, thereby reducing your CUR and improving your credit score. You can undo this benefit by going out and spending a large portion of your new credit limit right away.

Credit history age: The length of your personal credit history makes up 15% of your FICO score. A new card reduces the age of your average and newest account, a slight negative for your credit score.

Credit mix: If the new credit card is also your first credit card, then getting it broadens your credit mix. That’s a good thing, affecting 10% of your FICO score. The rule for credit mix is the more diverse, the better.

New credit: Most likely, the credit card company issuing your new credit card did a hard inquiry on your credit report before approving your application. New credit accounts for 10% of your FICO score, and each hard inquiry can drop your score by five to 10 points for up to a year.

In general, it’s a good idea not to get credit cards you don’t need. On the other hand, do not close accounts you no longer use, as this can raise your credit utilization ratio and hurt your credit score.

15. Do Instant Approval Cards Require a Credit Check?

When you apply for an instant approval card, the issuer might conduct two different credit checks. First, there’s a soft credit inquiry, which gives the issuer limited access to your personal credit history. This, along with other data, helps the issuer preapprove or prequalify your application.

This soft credit check is not visible to others who view your credit report and has no effect on your credit score. You don’t need to give the issuer permission to perform the soft check. Assuming you are preapproved and you agree to go forward, the issuer will next perform a hard inquiry.

The hard inquiry impacts your credit score for up to a year, although it remains visible on your credit report for two years. You must explicitly give the issuer permission to make a hard inquiry. The damage to your score is minimal, usually in the five- to 10-point range.

16. Can I Perform a Balance Transfer on an Instant Approval Card?

Most credit cards, no matter how long approval takes, give you the ability to transfer balances. But only a subset of cards provides an introductory 0% APR to new cardmembers. If you’re considering a balance transfer, you definitely want a card with the introductory offer.

Balance transfers help you consolidate your credit card debt so you face only one monthly payment with one minimum amount. It lets you concentrate on paying off the balance transfer card and thereby improve your credit score. Be aware of any balance transfer fees that may be imposed.

17. How Do I Request a Credit Limit Increase?

You can phone a customer rep to request an increase or take the impersonal approach online. Another approach is to simply wait; Some cards, especially secured cards and cards aimed at consumers with bad credit, may automatically offer you a higher limit after you exhibit creditworthy behavior for six months or longer.

Whichever approach you choose, always couch the request in terms of why you deserve it, not why you need it.

Ammunition for your request can include your spotless record of on-time payments, your higher income and/or lower expenses, your new job, or your desire for a balance transfer. The worst that can happen is that you’ll be turned down — the request should have no effect on your credit history.

For secured cardholders, the higher limit won’t require an additional security deposit to your collateral account.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

The information on this page was reviewed for accuracy on .

About the Author

Eric Bank

Finance Expert

Eric Bank is an M.B.A. who has covered financial and business topics since 1985, appearing regularly on Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences, particularly in the world of personal finance. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.

Share the Knowledge!

Our finance experts work hard to show you the best credit cards. Want to show your appreciation? Share this page!

Advertiser Disclosure: The credit card offers that appear on this site are from credit card companies from which CardRates.com receives compensation. This compensation may impact how and where products appear on this site (including, for example, the order in which they appear). CardRates.com does not include all credit card companies or all available credit card offers. See the credit card issuer's website for specific terms and conditions of each card.