Writer: Adam West

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

Shopping for a credit card isn’t quite as exciting as going shopping with a credit card — but you can’t do one without the other. And both require a bit of research and rational thinking if you want to avoid making a bad financial decision that could haunt you for years.

Thankfully, many major credit card issuers offer pre-qualifying applications that make it easier to narrow your choices and limit the hard inquiries placed on your credit report. And what’s even better, pre-applying for a credit card using one of these applications won’t hurt your credit rating.

Let’s take a look at a wide range of credit card pre-approval links from some of the most well-known issuers in the US Our list also includes credit cards with consumers in mind who have less-than-stellar credit.

-

Navigate This Article:

Credit Card Pre-Approval for Capital One

Capital One is among the most prolific credit card issuers in America, with more than 100 million cards in circulation. But just because everyone seems to have a Capital One card doesn’t mean the credit card company approves every applicant.

Instead of blindly applying for any Capital One card, you’re better served if you pre-qualify for one of the issuer’s offerings. The brief application requires basic information to identify the applicant — name, address, date of birth, and Social Security number.

You can also choose which type of card most interests you — be it a travel rewards, cash back, or low-interest rate card. You don’t have to answer this question if you have no preference. Just remember that Capital One limits consumers to only two cards from the issuer, so if you already have a pair of the company’s cards, you’ll likely receive a rejection for any application you submit.

Capital One will let you know if you pre-qualify for any of its cards a few moments after submitting your application. You’ll see which card(s) match your credit profile and the benefits related to each offering.

By doing this, you’ll limit your applications — and research — to only the cards you’re likely to be approved for. You may receive approval for one of our top-rated Capital One credit cards — which offer competitive interest rates and rich rewards. Check them out below.

- Earn a bonus of 20,000 miles once you spend $500 on purchases within 3 months from account opening, equal to $200 in travel

- $0 annual fee and no foreign transaction fees

- Earn unlimited 1.25X miles on every purchase, every day

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Transfer your miles to your choice of 15+ travel loyalty programs

- Enjoy 0% intro APR on purchases and balance transfers for 15 months; 18.49% - 28.49% variable APR after that; balance transfer fee applies

- Top rated mobile app

- Earn a one-time $200 cash bonus after you spend $500 on purchases within 3 months from account opening

- Earn unlimited 1.5% cash back on every purchase, every day

- $0 annual fee and no foreign transaction fees

- Earn unlimited 5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

- No rotating categories or sign-ups needed to earn cash rewards; plus, cash back won't expire for the life of the account and there's no limit to how much you can earn

- 0% intro APR on purchases and balance transfers for 15 months; 18.49% - 28.49% variable APR after that; balance transfer fee applies

- Top rated mobile app

- Earn a one-time bonus of 75,000 miles once you spend $4,000 on purchases within 3 months from account opening, equal to $750 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app

Credit Card Pre-Approval for Discover

Discover is one of the fastest-growing credit card issuers in America, thanks to its top-notch customer service ratings. Offering rich rewards is nothing new to Discover, as it was the first true rewards credit card when Sears launched the brand in 1986.

The issuer’s pre-qualifying application is a little longer than the average form. Discover asks about your current income, living situation, and bank account status, but the information helps the company decide which cards to match you with.

If the bank does approve you for one of its credit cards, you could end up reaping some huge rewards — like the ones offered by our top-rated cards below.

- INTRO OFFER: Unlimited Cashback Match for all new cardmembers. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards. You could turn $150 cash back into $300.

- Earn 5% cash back on everyday purchases at different places you shop each quarter like grocery stores, restaurants, gas stations, and more, up to the quarterly maximum when you activate. Plus, earn unlimited 1% cash back on all other purchases.

- Redeem cash back for any amount. No annual fee.

- 0% intro APR on purchases and balance transfers for 15 months; 17.49% - 26.49% variable APR after that; balance transfer fee applies.

- Terms and conditions apply.

- UNLIMITED BONUS: Unlimited mile-for-mile match for all new cardmembers. Discover gives you an unlimited match of all the miles you’ve earned at the end of your first year. There’s no signing up, no minimum spending or maximum rewards. Just a mile-for-mile match. You could turn 35,000 miles into 70,000 miles.

- Automatically earn unlimited 1.5x miles on every dollar of every purchase

- No annual fee.

- Turn miles into cash. Or redeem as a statement credit for your travel purchases like airfare, hotels, rideshares, gas stations, restaurants, and more. Redemption rates for these options may vary and are subject to change.

- 0% intro APR on purchases and balance transfers for 15 months; 17.49% - 26.49% variable APR after that; balance transfer fee applies.

- Terms and conditions apply.

- INTRO OFFER: Unlimited Cashback Match for all new cardmembers. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards.

- Earn 2% cash back at Gas Stations and Restaurants on up to $1,000 in combined purchases each quarter, automatically. You'll still earn unlimited 1% cash back on all other purchases.

- Get a 0% intro APR for 18 months on balance transfers. Then 17.49% to 26.49% Standard Variable APR applies, based on credit worthiness.

- Redeem cash back for any amount

- No annual fee.

- Terms and conditions apply.

Credit Card Pre-Approval for Chase

Many consumers choose Chase cards because of the ultra-attractive Chase Ultimate Rewards program, which gives cardholders a wide array of rewards options that range from travel to cash back and merchandise.

Chase has notoriously high standards for approval, which makes pre-qualifying a smart decision. But Chase requires you to sign in to your Chase account to “Browse offers selected for you based on your relationship with Chase.” If you don’t already have a relationship with the bank, you can create an account and see which card offers it suggests, if any.

Not only will you need good-to-excellent credit for Chase to consider your application, (unless you’re a student, in which case you may qualify for the Chase Freedom® Student credit card without a credit history) but you’ll also have to pass the issuer’s 5/24 rule.

This rule states that if you have opened five or more new bank card accounts (credit or charge cards) within the last 24 months, you’ll most likely be rejected when applying for a new Chase credit card — even if you otherwise qualify.

Here are the issuer’s three most popular rewards cards, along with links to each card’s easy online application:

- Intro Offer: Earn a $200 Bonus after you spend $500 on purchases in your first 3 months from account opening

- Enjoy 5% cash back on travel purchased through Chase Travel℠, our premier rewards program that lets you redeem rewards for cash back, travel, gift cards and more; 3% cash back on drugstore purchases and dining at restaurants, including takeout and eligible delivery service, and 1.5% on all other purchases.

- No minimum to redeem for cash back. You can choose to receive a statement credit or direct deposit into most U.S. checking and savings accounts. Cash Back rewards do not expire as long as your account is open!

- Enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 18.99% - 28.49%.

- No annual fee – You won't have to pay an annual fee for all the great features that come with your Freedom Unlimited® card

- Keep tabs on your credit health, Chase Credit Journey helps you monitor your credit with free access to your latest score, alerts, and more.

- Member FDIC

Additional Disclosure: Non-Monetized. The information related to Chase Freedom Unlimited® was collected by CardRates and has not been reviewed or provided by the issuer of this product/card. Product details may vary. Please see issuer website for current information. CardRates does not receive commission for this product.

- Earn a $200 Bonus after you spend $500 on purchases in your first 3 months from account opening.

- 5% cash back on up to $1,500 in combined purchases in bonus categories each quarter you activate. Enjoy new 5% categories each quarter!

- 5% cash back on travel purchased through Chase Ultimate Rewards®, our premier rewards program that lets you redeem rewards for cash back, travel, gift cards and more

- 3% cash back on drugstore purchases and dining at restaurants, including takeout and eligible delivery service, and unlimited 1% cash back on all other purchases.

- No minimum to redeem for cash back. You can choose to receive a statement credit or direct deposit into most U.S. checking and savings accounts. Cash Back rewards do not expire as long as your account is open!

- 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 19.24% - 27.99%.

- No annual fee - You won't have to pay an annual fee for all the great features that come with your Freedom Flex℠ card

- Keep tabs on your credit health - Chase Credit Journey helps you monitor your credit with free access to your latest score, real-time alerts, and more.

Additional Disclosure: Non-Monetized. The information related to Chase Freedom Flex℠ was collected by CardRates and has not been reviewed or provided by the issuer of this product/card. Product details may vary. Please see issuer website for current information. CardRates does not receive commission for this product.

- Earn 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening.

- Enjoy benefits such as 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases

- Earn up to $50 in statement credits each account anniversary year for hotel stays through Chase Travel℠

- 10% anniversary points boost - each account anniversary you'll earn bonus points equal to 10% of your total purchases made the previous year.

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Collision Damage Waiver, Lost Luggage Insurance and more.

- Complimentary DashPass which unlocks $0 delivery fees & lower service fees for a min. of one year when you activate by 12/31/27. Plus, a $10 promo each month on non-restaurant orders.

- Member FDIC

Additional Disclosure: Non-Monetized. The information related to Chase Sapphire Preferred® Card was collected by CardRates and has not been reviewed or provided by the issuer of this product/card. Product details may vary. Please see issuer website for current information. CardRates does not receive commission for this product.

Credit Card Pre-Approval for Citi

While most credit card issuers arm wrestle with each other to see who offers the richest rewards, Citi has quietly built a reputation for offering cards that help consumers eliminate debt fast while reducing interest fees and other charges.

This is most evident in the Citi Simplicity® Card, which offers an unheard-of introductory 0% interest period on balance transfers, though a balance transfer fee will apply. If you have an existing credit card balance that’s only growing because of interest charges, Citibank may have the solution to help you knock the debt out faster and more cheaply.

And Citi also has one of the easiest pre-qualifying applications to complete. Simply provide your name, address, and the last four digits of your Social Security number, and the bank will show you all of its cards that you may qualify for.

Those cards could include the popular offering above, or maybe another of our top-rated choices listed below.

- Earn 75,000 bonus Points after spending $6,000 in the first 3 months of account opening.

- Earn 12 Points per $1 spent on Hotels, Car Rentals, and Attractions booked on cititravel.com and 6 Points per $1 spent on Air Travel booked on cititravel.com

- Earn 6 Points per $1 spent at Restaurants including Restaurant Delivery Services on CitiNights℠ purchases, every Friday and Saturday from 6 PM to 6 AM ET. Earn 3 Points per $1 spent any other time

- Earn 1.5 Points per $1 spent on All Other Purchases

- Up to $300 Annual Hotel Benefit: Each calendar year, enjoy up to $300 off a hotel stay of two nights or more when booked through cititravel.com.

- No Foreign Transaction Fees

Additional Disclosure: Citi is a CardRates advertiser.

- Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

- Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 17.49% - 27.49%, based on your creditworthiness.

- Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

- If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Additional Disclosure: Citi is a CardRates advertiser.

- Earn 20,000 bonus Points after spending $1,000 in the first 3 months of account opening.

- 0% Intro APR on balance transfers and purchases for 15 months; after that, the variable APR will be 18.49% - 28.49%, based on your creditworthiness. There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

- Earn 3 ThankYou® Points for each $1 spent in an eligible Self-Select Category of your choice (Fitness Clubs, Select Streaming Services, Live Entertainment, Cosmetic Stores/Barber Shops/Hair Salons, or Pet Supply Stores). Choose your eligible Self-Select Category on Citi Online or by calling customer service. The default Self-Select Category is Select Streaming Services.

- Earn 5 ThankYou® Points for each $1 spent on Hotels, Car Rentals and Attractions booked on Citi Travel® via cititravel.com; earn 3 ThankYou Points for each $1 spent at Supermarkets, on Select Transit purchases, and at Gas & EV Charging Stations.

- Earn 2 ThankYou® Points for each $1 spent at Restaurants; earn 1 ThankYou® Point for each $1 spent on All Other Purchases.

- No Annual Fee

Additional Disclosure: Citi is a CardRates advertiser.

Credit Card Pre-Approval for American Express

American Express is known for being an ultra-selective credit card issuer. You must have at least good credit to qualify for any of its cards — there are no student offers or cards for bad credit available. But you can check to see if you pre-qualify for any of its cards on its website in as little as 30 seconds.

American Express is also known for issuing charge cards, which are credit cards with no preset spending limit. These cards must be repaid in full each month unless you select purchases to repay over time — with interest — in the app or on the issuer’s website.

Amex has lucrative signup bonuses and rewards card offers, not to mention a great lineup of business credit card options. Below are our expert’s top-rated Amex cards, all available to consumers with good to excellent credit:

Credit Card Pre-Approval for Bad Credit

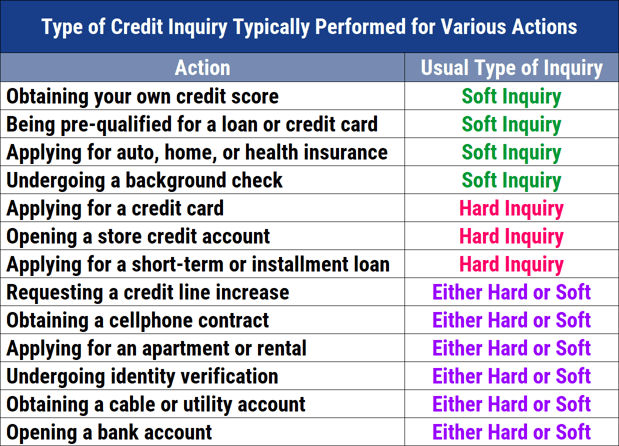

If you’re dealing with bad or no credit, getting pre-qualified for a credit card could be a game-changer in your research process. Why? Every official credit card application you submit triggers a hard inquiry on your credit report. These inquiries tell lenders that you’re in the market for a loan or line of credit.

That may seem harmless enough, but if you accrue several of these marks on your credit file, lenders may see you as a higher credit risk. Each inquiry can bring your credit score down — and a lower credit score makes it even harder to qualify for a credit card.

Most credit scoring models tolerate two or three hard inquiries on your report over a two-year span. However, exceeding that number can harm your score.

In contrast, a prequalifying application only involves a soft inquiry, which doesn’t impact your credit score and provides a clearer picture of the cards you might qualify for.

Many credit card issuers collaborate with people who want to boost or build their credit scores. Fortunately, they often offer pre-qualifying applications to speed up and ease the approval process.

Check out our top options below for more cards that make it easier to rebuild — or establish — your credit profile.

- Up to $1,000 Initial Credit Limit

- See if you Pre-Qualify with No Impact to your Credit Score

- Less than perfect credit? We understand. The Surge Mastercard is ideal for people looking to rebuild their credit.

- Unsecured credit card requires No Security Deposit

- Perfect card for everyday purchases and unexpected expenses

- Monthly reporting to the three major credit bureaus

- Use your card everywhere Mastercard is accepted at millions of locations

- Enjoy peace of mind with Mastercard Zero Liability Protection for unauthorized purchases (subject to Mastercard guidelines)

- Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

+ See More Credit Cards for Bad Credit

Which Credit Cards Offer Pre-Approval?

When you’re on the hunt for a credit card, it’s smart to focus on issuers that offer pre-approval applications rather than specific cards. That’s because an issuer’s application might connect you with multiple cards you qualify for.

And like most things in life, there’s strength in numbers.

Take, for example, Capital One. By filling out the bank’s pre-approval application, you could receive several offers and then decide which one best matches your needs. If you go into your research with your heart set on one specific card, you increase the chance of being disappointed if you don’t qualify for that card.

Your best first step is to decide what matters most to you in a credit card. From there, you can decide which issuer offers the best options to fit your desires and attempt to pre-qualify with that bank.

If you’re looking for rewards, you may decide to pre-apply with Chase or Discover. If you need a good balance transfer card, or a card with a longer 0% introductory period, then you may want to consider Citi. Whichever you choose, keep your options open.

What’s the Difference Between Pre-Approved and Pre-Qualified?

Both terms sound very different but have very similar meanings.

Once upon a time, pre-approved meant the credit card issuer reviewed a soft pull of your credit report and would offer you a credit card if you decided to apply. That’s no longer the case.

Credit card issuers purchase large batches of consumer data from credit reporting bureaus. They use their filters to decide which consumers might meet their minimum standards for approval. They may give specific criteria to the bureau and receive several thousand credit files that meet those criteria. That’s how they choose who receives those pre-approval letters in the mail.

But they don’t actually guarantee approval — pre-approval is more of an invitation to apply for a credit card. It’s the issuer’s way of saying “You look like you might be a good match for our card. Feel free to apply, and we’ll see if we’re right.”

An issuer can’t promise approval until they thoroughly review your complete credit file. And that’s only possible once you apply.

So, even though you may think you’re pre-approved, the issuer could see something when it pulls your credit report that wasn’t visible before. And that could lead to a rejection or less attractive terms than what your pre-approval letter offered.

Still, many experts believe that receiving a pre-approval offer gives you about a 90% chance of getting the card if you go ahead and apply.

Pre-qualifying offers are quite similar, but the outcome remains uncertain. Credit card issuers send out millions of these letters every year, yet only some of the recipients will actually qualify for the card being offered.

That’s because the credit profile data used to determine pre-qualifications is far broader than the information used for pre-approvals. An issuer may purchase a batch of credit profiles, for example, with credit scores between 650 and 800, and send offers to everyone on the list.

Or, the issuer may apply a filter for consumers who haven’t had a late payment in the last three months. All of this information is useful, but not definitive.

Does Credit Card Pre-Approval Affect Credit Scores?

No, credit card pre-approval does not affect your credit scores. Credit card pre-approval is done through a soft pull of your credit report, which does not appear on your credit history.

If you decide to apply for the card after receiving pre-approval, you will obtain a hard inquiry, which will appear on your credit history and may affect your credit score for up to one year, but only by a few points. The fear of obtaining a hard inquiry isn’t reason enough to avoid applying.

That’s because the new credit limit you receive upon approval may improve your credit, so you may not feel any negative effects from the inquiry. An increase in the amount of credit available to you can help lower your credit utilization if you have other credit card debt, or it may broaden your credit mix if this is your first credit card.

The impact of getting a credit card can vary significantly depending on your unique financial situation. We can’t predict exactly what will happen because it all depends on your personal credit history.

Can You Be Denied a Pre-Approved Credit Card?

As we mentioned earlier, pre-approval isn’t a sure thing. The offers you get are based on the version of your credit file that the lender checked, which often happens a month or two before you even receive the offer.

A lot can happen in two months. If you’ve experienced any major changes to your credit score during that time, it could greatly impact your chances of final approval.

Even if your credit report doesn’t change in that time frame, you could still find yourself with a rejection, despite the pre-approval. That’s because the issuer doesn’t always examine every part of the soft credit pull before sending you an invitation to apply.

For example, the issuer may look for consumers who haven’t missed a payment in six months. That could trigger tens of thousands of letters sent to consumers across the country. But when one applies, and the issuer sees that he or she has three maxed-out credit cards, it likely won’t end in an offer.

That’s why pre-qualifying applications can be really helpful if you use them carefully. On the plus side, they might help you dodge rejection when you officially apply for a card. However, they can also create a false sense of confidence that you’ll secure a specific card, even if you might not qualify otherwise.

The most effective way to truly understand your credit report is to check it yourself. The government offers each consumer one free credit report every week from each credit reporting bureau. While these reports won’t display your actual credit score, they will show all the essential information credit card issuers review when evaluating your application.

Before applying for a new credit card, make sure your reports are up-to-date and accurately represent your financial status. Think of your application as a blind date. The issuer doesn’t know you or your history, but you can make a great impression by understanding your credit report and taking steps to improve it before introducing yourself to the bank.

Reduce Your Chances of Rejection By Receiving Pre-Approval

Think of credit cards like cookies. They’re delicious and easy to grab, but tough to resist. Applying for credit cards can feel the same way. If you’ve faced rejection, you might be tempted to try for another card.

But, like cookies, the more applications you submit, the less satisfying the results. You can avoid collecting hard inquiries on your credit report by filling out a pre-qualifying application to the issuer of your choice. Not only will it give you a clearer picture of your finances, but it’ll keep those pesky inquiries at bay.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

![Discover Card Pre-Approval: 4 Best Offers to Prequalify[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2016/09/discover-pre-approved.jpg?width=158&height=120&fit=crop "Discover Card Pre-Approval: 4 Best Offers to Prequalify[updated_month_year before=\" (\" after=\")\"]")

![3 Steps to Credit One Pre-Approval[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2016/11/CreditOneApp.png?width=158&height=120&fit=crop "3 Steps to Credit One Pre-Approval[updated_month_year before=\" (\" after=\")\"]")

![18 Best Pre-Approval Credit Cards: 100% Online[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/09/preapprove-23.png?width=158&height=120&fit=crop "18 Best Pre-Approval Credit Cards: 100% Online[updated_month_year before=\" (\" after=\")\"]")

![Capital One Pre-Approval: 5 Secrets to Prequalify[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2016/05/capital-one-pre-qualify-1.png?width=158&height=120&fit=crop "Capital One Pre-Approval: 5 Secrets to Prequalify[updated_month_year before=\" (\" after=\")\"]")

![Chase Pre-Approval: 6 Best Offers to Prequalify[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/05/chase.png?width=158&height=120&fit=crop "Chase Pre-Approval: 6 Best Offers to Prequalify[updated_month_year before=\" (\" after=\")\"]")

![7 Best Pre-Approval Auto Loans[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2023/10/Best-Pre-Approval-Auto-Loans.jpg?width=158&height=120&fit=crop "7 Best Pre-Approval Auto Loans[updated_month_year before=\" (\" after=\")\"]")

![5 Pre-Qualified Credit Cards For Bad Credit[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2020/03/Pre-Qualified-Credit-Cards-for-Bad-Credit.jpg?width=158&height=120&fit=crop "5 Pre-Qualified Credit Cards For Bad Credit[updated_month_year before=\" (\" after=\")\"]")

![[card_field card_choice='5854' field_choice='title'] Credit Limit & Pre-Qualifying[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/10/shutterstock_662150614.jpg?width=158&height=120&fit=crop "[card_field card_choice='5854' field_choice='title'] Credit Limit & Pre-Qualifying[updated_month_year before=\" (\" after=\")\"]")