Eric Bank is an M.B.A. who has covered financial and business topics since 1985, appearing regularly on Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences, particularly in the world of personal finance. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.

Ashley Fricker has more than a decade of experience as a finance contributor and editor, and has specialized in the credit card industry since 2015. Her credit card commentary is featured on national media outlets that include CNBC, MarketWatch, Investopedia, and Reader's Digest, among many others. She has worked closely with the world’s largest banks and financial institutions, up-and-coming fintech companies, and press and news outlets to curate comprehensive content and media. Ashley holds a bachelor's degree in multimedia journalism from Florida Atlantic University.

With more than 10 years of accounting experience, Danielle Marshall has a deep understanding of many financial disciplines, including personal and commercial lending, retirement annuities, financial forecasting, and general bookkeeping. She has a bachelor's degree from the University of Florida's Fisher School of Accounting and currently manages all accounts receivable and payable for the parent company of CardRates.com. She works directly with credit card issuers and advertising partners to ensure our content meets compliance expectations and regulatory standards.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our Rating

Total Visa® Card

3.8/5.0

About this rating

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

The Total Visa® Card is available to consumers with bad credit, including those who’ve recently emerged from bankruptcy. It offers cash back rewards, and you can use it to rebuild credit with responsible use and consistent on-time payments. But it saddles you with many nuisance fees and a high interest rate, which is typical of unsecured cards for bad credit.

In this review, we evaluate the card and three of its competitors. There may be less-expensive credit cards out there that cater to folks with poor credit, but that’s up to you to decide (with our guidance).

The Total Visa® Card aims for consumers with less-than-perfect credit. It is an unsecured card, so you don’t have to lay out a security deposit. You earn 1% cash back on eligible purchases, receive free credit monitoring, and have access to a user-friendly mobile app.

The credit card issuer, the Bank of Missouri, understands that those who apply for the card are risky customers. Having poor credit indicates higher-than-average odds that you’ll default on your card within two years. That’s why the issuer offers a small credit limit and requires more than half of that amount in upfront fees.

The card charges a one-time program fee, an annual fee, and, starting in the second year, fees for monthly servicing and cash advances. There are also fees for late or returned payments, and the 35.99% APR is high. But you can avoid the card’s hefty interest charges by paying your balance in full each month.

How to Qualify & Apply

You can get the Total Visa® Card even if you have really poor credit. But you must be a US resident, 18 or older, with a bank account and enough income to afford the monthly minimum payments. You can learn more below and apply on the bank’s website by clicking the Apply Now button:

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

^^1% Cash Back is earned on payments to your Credit Card. Up To 10% Cash Back is earned on qualifying purchases at select participating merchants. Offer percentages vary by merchant and are subject to change. See Total Card Visa Rewards Programs Terms & Conditions for details

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APR35.99%

Annual FeeSee Terms

Credit NeededFair, Bad Credit

The online application collects information that includes:

Name

Date of birth

Address

Phone number

Email address

Bank account

Social Security number

Employer contact data

How long you’ve lived at your current residence

Pay amount and frequency

Estimated total monthly expenses

The application lets you select a card design, including a premium option for a fee. It asks whether you want to sign up for Payment Guard Plus, an optional, fee-based program to cover your payments when certain qualifying events occur (i.e., death, job loss, hospitalization, disability, and auto or medical expenses).

You also must indicate whether you already have a credit or debit card, plan to take cash advances, and want to authorize an additional cardholder. The Total Visa® Card should give you a decision within a few moments and, if favorable, will ask you to e-sign the cardmember agreement.

You must pay the one-time setup fee before the issuer mails you your new card. The annual fee of See Terms, reduces your initial credit limit until you pay it.

You may also receive a preapproval letter from the bank with a reservation code you can enter online when you apply for the card. The credit card issuer makes these prescreened offers based on information in your credit reports indicating that you meet certain criteria.

These mail offers do not guarantee approval — you must continue to satisfy the issuer’s criteria. You’re not eligible for an offer if you already have the card or if you’ve applied in the last 60 days.

Benefits & Drawbacks

The card’s benefits include cash back rewards, minimal credit requirements, and reporting to the credit bureaus. Drawbacks include prohibitive costs and tight credit limits.

Benefits

Earn 1% cash back on eligible purchases.

You’re protected against unauthorized charges.

Quick application with an immediate response, available to individuals with bad credit.

No upfront deposit is required.

Potential credit limit increases.

Credit reporting to all three major credit bureaus to help you build credit with responsible use.

Drawbacks

High 35.99% APR

One-time program fee upon account opening.

High annual fee, See Terms

Monthly servicing fee, billed after the first year

Fees for late payments, cash advances, additional cards, premium designs, and other transactions.

You must wait 90 days before you can qualify for a cash advance.

There is a fee for approved credit limit increases. You must wait at least one year before receiving an increase.

The card’s overall cost/benefit profile is not optimal. Please consider your other options, including the three cards reviewed next.

Similar Cards to Consider

The following cards provide benefits similar to those of the Total Visa® Card but may cost less to own or offer higher credit limits. The things to look for are the initial credit line, annual fee, interest rate, and whether you can earn rewards. Evaluating those points should help lead you to the right decision.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

The Milestone® Mastercard® caters to those who have Fair to Good credit. Pay your monthly payment on time and reporting to the credit bureaus can help improve your scores rise over time. There’s no security deposit required, and the card’s starting credit limit is $700.

The card offers a few other essential benefits, including a mobile app and fraud protection.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Earn Cash Back Rewards* – 3% on Eligible Gas, Groceries, and Utilities, and 1% on All Other Eligible Purchases

Use Anywhere Mastercard is Accepted

No Security Deposit

$0 fraud liability**

Free access to your Credit Score†

*See Program Terms for important information about the cash back rewards program.

**Fraud liability subject to Mastercard rules.

† Your credit score will be available in your online account starting 60 days after your account is opened. (Registration required.) The free VantageScore 4.0 credit score provided by TransUnion® is for educational purposes only. This score may not be used by The Bank of Missouri (the issuer of this card) or other creditors to make credit decisions.

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APR36% Fixed

Annual Fee$85-$175 first year, $229 thereafter

Credit NeededPoor, Fair, or No Credit

The Fortiva® Cash Back Rewards Mastercard offers bonus cash back on gas, groceries, and utility bill payments and 1% on all other purchases. The card provides an initial credit limit of up to $1,000 and does not charge a setup fee. It is one of the few cards in this category that offer balance transfers (fees apply).

You also receive free transaction alerts, credit score tracking, and $0 fraud liability coverage. The APR depends on your creditworthiness while the annual fee is based on your approved credit limit, which also determines your account maintenance fee.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Less than perfect credit? We understand. The FIT Mastercard is ideal for people looking to rebuild their credit.

Unsecured credit card requires No Security Deposit

Perfect card for everyday purchases and unexpected expenses

Monthly reporting to the three major credit bureaus

Use your card everywhere Mastercard is accepted at millions of locations

Enjoy peace of mind with Mastercard Zero Liability Protection for unauthorized purchases (subject to Mastercard guidelines)

If approved, you must pay a $95 fee to open your account. Please see the terms and conditions for when you apply.

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APR35.90% Fixed

Annual FeeSee terms

Credit NeededFair/Poor/Bad

You can use the FIT™ Platinum Mastercard® to help rebuild your credit with consistent on-time payments because it reports your account to all three credit bureaus. It doesn’t offer cash back rewards, and it might not provide a higher initial credit limit than the Total Visa® Card.

The card’s APR is no bargain but is appreciably lower than that of the Total Visa® Card. Of course, both cards offer a 0% APR by paying your total balance each month.

Cardholder Reviews Around the Web

Here are a couple of representative comments from the online forums regarding the Total Visa® Card.

“I have the card, and I have had no problems with it. Yes, I paid the fee upfront, but everything has been cool so far. Customer service is good. I make a payment, and it posts the next day. There is no interest because I pay in full if I charge something. I would say keep it for 6 months and close it. That’s my plan.”

“Don’t get it. It’s not worth it. I have had this card for 4 years & 3 months. It STILL only has a limit of $350. They refuse to budge. I started at $250…The customer service is terrible. The website isn’t great, but at least they don’t charge me to make a payment. Which by the way, I can only do once every 10 days. This card will definitely NOT grow with you.”

Just about every credit card receives good and bad comments on the internet. Those for Total Visa® Card are fairly typical of unsecured cards for poor credit.

FAQs: What is the Card’s Credit Limit?

The initial credit limit tops out at $500. The card does not permit credit line increases during the first 12 months of account ownership.

All increases trigger a fee based on the increase amount. If you need help finding the bottom of the barrel, just look for cards that charge this fee.

Eventually, you may be able to achieve a credit limit of $1,000 or so, but it’s a much better idea to pay your bills on time to potentially help improve your credit and then get a less expensive credit card down the road.

The credit limit on cash advances is 50% of your total limit. Note that you must wait three billing cycles before you can take a cash advance. The card does not support balance transfers.

How Do I Build Credit with the Card?

The bank reports your payments to all three major credit bureaus. Triple reporting is the most efficient way to build credit, but only if it reports creditworthy behavior, starting with on-time payments every month.

The FICO and VantageScore algorithms recognize timely payments and will calculate your scores accordingly. It may take a year to make meaningful progress. Still, eventually, you’ll gain access to better credit cards and cheaper loans.

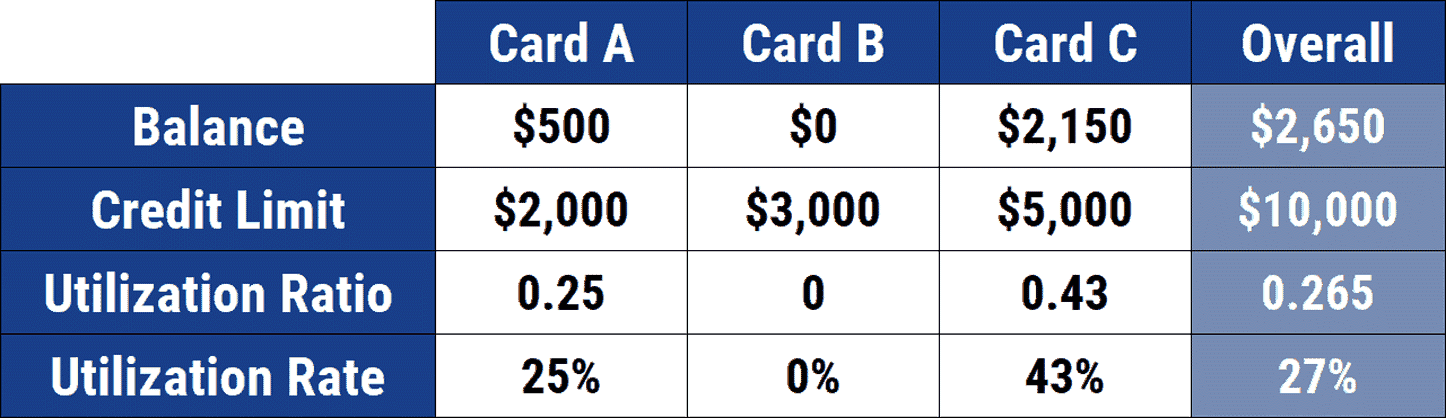

It’s also essential to keep your debt levels low. You want to maintain your credit utilization ratio as small as possible but at least no greater than 30%. CUR is the amount of credit card credit you are currently using divided by your total credit limit.

Example of credit utilization across three card accounts.

You can maintain a 0% CUR by paying your balance in full each month, with the extra benefit of avoiding interest charges.

Credit card accounts also build credit simply by aging. The credit scoring algorithms track the age of each account as well as the average and oldest age. A long credit history shows that you can manage your finances responsibly, and your credit history will benefit. Ideally, you’d like to have at least one account that is seven or more years old.

Does the Total Visa® Card Have a Mobile App?

Yes, and its mobile application gives cardholders a quick and straightforward way to manage their credit card accounts. The app allows you to:

The app provides several data privacy features, including the following:

The app does not share user data with third parties (i.e., other companies or organizations).

The collected data consists solely of app info and performance, device ID, personal information, and payments.

The app encrypts the data in transit.

You can request the app developer to delete data.

You can download an Apple or Android version of the card’s mobile app.

Would a Secured Card Be Better than this Card?

Secured cards are usually a better option than high-priced unsecured cards if you have poor credit. While it’s true that you must lay out a deposit for a secured card, you’ll get a refund when you close or upgrade the account. Whereas the ridiculous fees that many subprime unsecured cards charge are sunken money, gone forever.

In addition, secured cards typically have lower interest rates and better perks. You control the credit limit by the amount of your deposit. Secured cards are easy to get despite having no, limited, or poor credit.

Total Visa® Card

Typical Secured Card

Credit Check

Required but lenient

Often required but less stringent

Initial Fee

High program fee

Usually, no program fee

Annual Fee

See Terms

Typically $0

APR

35.99%

Usually much lower

Credit Limit

$500, reduced by fees

Set by the security deposit amount

Security Deposit

Not required

Required, refundable

Credit Limit Increase Fee

20% of the increase amount

None

Reporting to Bureaus

Yes

Yes

In a nutshell, you could spend $170 in upfront fees to get an unsecured card with a $500 credit limit. Or you could shell out a refundable $500 deposit on a secured card with no annual or program fees. Your money, your choice.

Can You Use the Card Right Away?

There is no way to use the account until you receive the card, which in turn depends on how quickly you pay the one-time program fee. The bank does not issue virtual account numbers nor release your account information before you physically receive and activate the card.

Expect the card to arrive in the mail within seven to 10 business days after your program fee payment clears.

Is the Total Visa® Card Worth It?

You have card options better than this card for building credit. Just about any secured credit card would be a superior deal, as we explained earlier. Also, the three reviewed alternative cards deserve consideration, as they may be less costly or provide a higher credit limit.

You should also consider getting a credit card from your local credit union. These organizations usually have member-friendly policies and products, although most credit unions restrict membership in some way.

For example, the cashRewards® Secured Credit Card from Navy Federal Credit Union is available to members who have ties to the military.

This Card May Be For You If…

You want to earn cash back rewards on all eligible purchases, which can help offset some of the card’s fees.

You need to build credit. It reports to the three major credit bureaus, which can help improve your credit when you make timely payments.

You want an unsecured credit card with relatively low credit requirements, suitable for consumers with bad credit.

You’ll want to weigh all your options before applying for the Total Visa® Card. Whichever card you choose, take the opportunity to build your credit through responsible use.

About the Author

Eric Bank is an M.B.A. who has covered financial and business topics since 1985. He has contributed regularly to Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org, and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.