Eric Bank is an M.B.A. who has covered financial and business topics since 1985, appearing regularly on Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences, particularly in the world of personal finance. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.

Jon leverages 15-plus years of journalism expertise to inform financial consumers about emerging trends and companies making an impact in the industry. He is most knowledgeable in the areas of budgeting, credit card rewards, and responsible credit use. Jon has a passion for writing and editing, and his articles have appeared in publications produced by The New York Times.

Ashley Fricker has more than a decade of experience as a finance contributor and editor, and has specialized in the credit card industry since 2015. Her credit card commentary is featured on national media outlets that include CNBC, MarketWatch, Investopedia, and Reader's Digest, among many others. She has worked closely with the world’s largest banks and financial institutions, up-and-coming fintech companies, and press and news outlets to curate comprehensive content and media. Ashley holds a bachelor's degree in multimedia journalism from Florida Atlantic University.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our Rating

Milestone® Mastercard®

3.8/5.0

About this rating

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Consumers with limited or bad credit can choose from dozens of subprime credit cards with undemanding credit requirements. Almost all members of this card group charge high fees and eye-watering interest rates, and the Milestone® Mastercard® is no different.

But it is an unsecured card that doesn’t require a security deposit and can help you improve your credit with responsible use over time. This can be achieved by always paying your bill on time and keeping a relatively low balance.

The question is: How does this card distinguish itself from other subprime cards, and is it your best option? Let’s find out.

The Milestone® Mastercard® caters exclusively to consumers who need to rebuild their credit.

This unsecured card has a relatively high credit line, and its lack of security deposit is attractive.

Its list of benefits is thin, and it doesn’t advertise any way to increase your credit limit over time.

It charges high fees and interest rates, but the interest is avoidable when you pay your bill within the interest-free grace period.

How to Qualify & Apply

To be eligible for the card, you must:

be 18 or older

reside in the United States

have a Social Security number, email address, and enough income to afford your monthly minimum payment

not have an existing Milestone credit card account, and the issuer will reject your application if it charged off a previous account due to delinquency.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Depending on your qualifications, the issuer may offer you one of three different card versions: Gold-300, Gold-301, or Gold-322. They differ in their annual fees but otherwise offer identical terms and conditions. You may need to provide some additional data to formally apply for the card.

Benefits & Drawbacks to Consider

This card has several benefits to help subprime borrowers access credit and increase their credit scores with responsible usage. Let’s look at the positives first:

Benefits

Easy approval: You can get the card even if you have poor credit. But your debt-to-income (DTI) ratio may trip you up if it’s too high.

No security deposit required: It is an unsecured credit card, so you don’t have to put down a security deposit.

Credit bureau reporting: The card reports your payments to all three major credit bureaus (Experian, TransUnion, and Equifax). Triple-reporting is the most efficient way to build credit, but only if you pay your bills on time.

It’s a genuine Mastercard: That means you get basic features such as $0 fraud liability protection.

Online account management: You have 24/7 access to your account so you can track your progress.

Credit line: You can get a decent credit line. It won’t be a fortune, but it may exceed that of some competitors.

Drawbacks

Annual fee: The card charges a yearly fee that depends on which card variety the issuer offers you.

No rewards: Many unsecured subprime cards don’t offer cash back or other rewards, and this one is no different.

No signup incentives: The card offers no signup bonus or introductory 0% APR promotion. That’s not unusual for a card of this type.

No path to a higher credit line: The card’s website doesn’t mention any way to increase your credit line over time. That’s unusual, even in the subprime card segment.

Minimum benefits: The card offers no consumer or travel benefits other than fraud liability protection.

Other Fees: The card charges fees for foreign transactions, cash advances, late/returned payments, and spending over the credit limit. But it does not charge a setup or monthly fee, unlike many of its competitors.

Potentially high APR: The card’s APR is about the highest legal APR a bank can charge, making its rate on the verge of predatory. But cardholders can avoid paying interest altogether by paying their balance in full each month.

We’d suggest considering a secured card, or one of the unsecured cards below, for better interest rates and potential purchase rewards.

Similar Cards Worth Your Attention

If you have bad credit, these three cards are worth considering and may provide better benefits than the Milestone® Mastercard®. One is from a major bank, and none require a security deposit for approval.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

No annual or hidden fees. See if you're approved in seconds

Be automatically considered for a higher credit line in as little as 6 months

Help build your credit through responsible use of a card like this

Enjoy peace of mind with $0 Fraud Liability so that you won't be responsible for unauthorized charges

Monitor your credit score with CreditWise from Capital One. It's free for everyone

Get access to your account 24 hours a day, 7 days a week with online banking from your desktop or smartphone, with Capital One's mobile app

Check out quickly and securely with a contactless card, without touching a terminal or handing your card to a cashier. Just hover your card over a contactless reader, wait for the confirmation, and you're all set

Pay by check, online or at a local branch, all with no fee - and pick the monthly due date that works best for you

Our research into the Capital One Platinum Credit Card has found reports of approvals for scores down to 570, and one Credit Karma reviewer reported receiving approval even after a recent bankruptcy. Others report approval with scores below 570, but these claims are self-reported, so we can’t verify them.

This card has benefits beyond its low minimum score, such as automatic consideration for a credit line increase after you make five monthly payments on time. Naturally, this doesn’t guarantee an increase, but many reviewers report boosts from $300 to $1,000 or more.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Many people consider the best feature of the Surge® Platinum Mastercard® to be its reporting to all three major credit bureaus. You can use the card to rebuild damaged credit as long as you maintain your card in good standing. The maximum credit limit is high enough to support a low credit utilization ratio.

Surge is an unsecured credit card, so you won’t need to put down a deposit or pre-load the card to use it. Its annual fee is relatively high, as is its APR. If you have a low FICO score and other cards won’t approve your application, you may have better odds with the Surge card.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

The Destiny Mastercard® helps you build credit when you pay on time by reporting to all three credit bureaus. It is a real Mastercard, welcomed at 40 million locations in-store, online, and in-app. The card provides fraud protection against lost and stolen cards. It’s an unsecured card, so you don’t have to pay a security deposit.

Unfortunately, its APR is ridiculously high, as is its first-year annual fee. The card also adds a monthly fee after the first year of ownership. The card’s issuer is The Bank of Missouri, and its servicer is Concora Credit, Inc., which explains the card’s similarities to the Milestone® Mastercard®.

FAQs: What is the Credit Limit on the Milestone® Mastercard®?

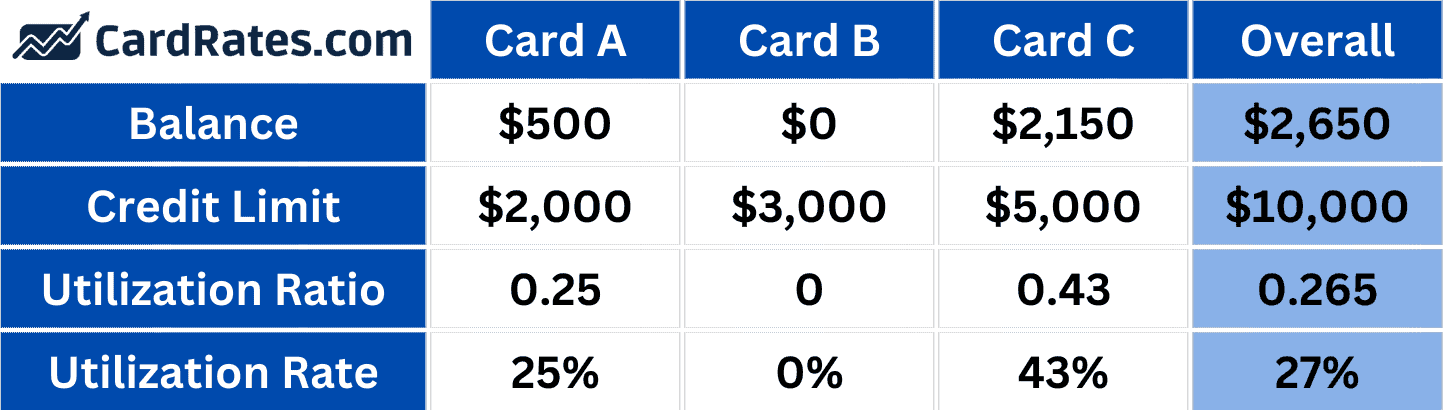

Reports of the card’s maximum credit limit range from $300 to $700. That’s a tight leash on your spending and may challenge your ability to maintain a low credit utilization ratio (i.e., your current balance divided by your credit limit).

Ideally, you want to maintain a CUR below 30%, which is a paltry $90 on a $300 limit. Worse, there isn’t a way to get a higher limit over time. Ideally, you will pay your entire balance each month — that’s the best way to maintain a low CUR and avoid interest charges.

Example of credit utilization calculated across three accounts.

The issuer requires you to refrain from using your account in any way that would cause you to go over your credit limit. It may refuse to authorize or accept any transaction that would cause you to exceed your limit, even if you have instructed the issuer to charge you an over-limit fee for doing so.

The Bank of Missouri may temporarily agree to allow you to exceed your credit limit. However, in that case, you must repay the excess amount immediately. Any transactions the card honors above your credit limit will leave your limit unchanged.

The issuer may, at any time and without prior notice, increase or decrease your credit limit, restrict the credit limit for cash advances, or take away your ability to obtain cash advances.

What Credit Score Do I Need to Apply?

The issuer doesn’t specify a minimum credit score required to apply, though it does indicate borrowers should have at least fair credit — a FICO score above 580 — for approval. We’ve surveyed the internet and found claims of acceptable minimum scores from 300 to 550.

That said, the card’s terms definitely lean toward being designed for people with poor credit, not fair or good credit. If your score is above 600, you can likely find a better card.

How am I Protected Against Fraud and Unauthorized Charges?

As a Mastercard cardholder, Zero Liability Protection applies to your purchases made over the telephone, in the store, online, or via a mobile device and ATM transactions. You will not be responsible for unauthorized transactions if:

You use reasonable care in protecting your card from loss or theft.

You promptly report the loss or theft to your financial institution.

By meeting these conditions, you are not liable for any charges arising from unauthorized use. If you suspect improper use of your card, call the number printed on the back of the card immediately.

ID Theft Protection

Identity theft occurs when a criminal uses your personal information (e.g., your name or Social Security number) without your permission to commit fraud or other crimes. These violations include:

Opening new credit accounts

Filing for a tax refund

Seeking medical treatment and obtaining prescriptions in your name

Filing for unemployment benefits in your name and intercepting the checks

Mastercard’s US-based, certified identity theft resolution specialists and online resources are available 24/7 to educate you about identity theft and provide tips to help you reduce risk.

Mastercard offers the following steps to help prevent ID theft:

You can opt out of receiving pre-approved credit card direct mail offers and marketing phone calls that thieves can use to steal your personally identifiable information.

If your identity is at risk, you can place a one-year fraud alert on your credit file, making it more difficult for thieves to open new credit in your name without your knowledge.

You can track your profile, access identity theft protection tips, and respond to alerts from the Mastercard web portal. Its easy-to-use online monitoring dashboard helps you take a more active role in protecting your identity.

You’ll receive monthly communications to stay up to date about common identity-related threats, as well as the services and protections you can use to protect yourself.

You can request Mastercard’s Identity Theft Protection Kit, which explains many forms of identity theft and provides prevention advice and resolution resources. This kit also contains a Federal Trade Commission sample affidavit form as well as sample letter templates for filing disputes in cases of identity theft or fraud.

Sign up for IDRiskIQ™, which helps you better understand your identity theft risk level and provides a personalized action plan to help you lower your risk of identity theft.

Unfortunately, even the most vigilant cardholders can fall victim to identity theft. If it happens to you, your Milestone® Mastercard® can offer several types of support, including the following:

Certified Identity Theft Resolution: Mastercard’s specialists are FCRA, CIPA, and CTRMS® certified and available 24/7/365 to help resolve your identity theft/fraud incident and prevent further damage. A specialist will perform all the tasks to restore your identity.

Identity Theft Affidavit Assistance and Submission: If someone compromises your identity, Mastercard will supply you with a pre-populated identity theft affidavit to dispute any fraudulent activity or claims. After helping you fill out the form, it will submit the affidavit to the appropriate authorities, creditors, and credit bureaus on your behalf.

Creditor Notification, Dispute, and Follow-Up: Mastercard will contact your creditors’ fraud departments with separate itemized account statements to dispute each fraudulent occurrence. It will also follow up with creditors to resolve each issue and provide you with updated status reports throughout the entire process.

Lost Wallet Assistance: Mastercard will assist you in notifying the appropriate bank or issuing authority to cancel and replace missing or stolen items, such as your driver’s license, debit/credit card(s), Social Security card, and passport.

Medical Identity Theft Assistance: If someone fraudulently uses your identity to obtain medical services and treatment, Mastercard will work with your insurers and healthcare providers to resolve the issues and correct your medical records/claims.

Final Thoughts

The Milestone® Mastercard® says it’s designed for people with fair or good credit, but its terms scream poor credit. Its rates and fees are the legal maximum a bank can charge, so it’s best to consider your alternatives before deciding to apply for this card.

Secured cards may provide better rewards and benefits than their unsecured counterparts, and they usually cost less. You will have to put down collateral, but the issuer will likely return it within six to 12 months. If your credit score is in the ditch and you can lay out the deposit money, a secured credit card may be your best bet.

About the Author

Eric Bank is an M.B.A. who has covered financial and business topics since 1985. He has contributed regularly to Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org, and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.