Writer: Adam West

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

Who can say no to a freebie, right? But let’s face it, most things in life come with a price. So, snagging an interest-free financing deal can feel like a pretty sweet perk.

You can save thousands of dollars with the right credit card that offers an extended interest-free introductory period. And whether you’re making a big purchase or paying off existing debt that’s currently sitting on a credit card with a high APR, there’s never been a better time to find the right 0% offer.

That’s because the competition between many credit card issuers has some banks offering new cardholders sweet deals — many of which are unprecedented in the space.

-

Navigate This Article:

Two Cards with No Interest on New Purchases for 18+ Months

The average credit card APR currently sits at 17.72%. Let’s say you make a $4,000 purchase on a new card at that rate. If you make monthly payments of $222.22, you’ll pay that debt off in 22 months — including $684.09 in interest charges.

With an 18-month interest-free credit card, you have the chance to pay off your balance over 18 months without any added finance charges. This means you could save almost $700 while tackling your debt faster.

But the pandemic changed credit card rewards a lot, and extended 0% purchase APRs are much harder to find than are 0% balance transfers. We know of just two cards that currently net you 18+ months of 0% APR on new purchases:

- For a limited time, get a special 0% introductory APR on purchases and balance transfers for 24 billing cycles. After that, the APR is variable.

- Earn 4% cash back on prepaid air, hotel and car reservations booked directly in the Travel Center when you use your card

- Get up to $600 reimbursement if your cell phone is stolen or damaged when you pay your monthly cell phone with your card

- View your credit score anytime, anywhere in the mobile app or online banking. It's easy to enroll, easy to use, and free to U.S. Bank customers.

- Get an opportunity to set up a 3-month $0 ExtendPay Plan offer each calendar year after the new account 0% introductory purchase APR offer has expired

- $0 Annual Fee

Additional Disclosure: The information related to this card has been collected by CardRates.com and has not been reviewed or provided by the issuer of this product.

New cardholders of the U.S. Bank Shield™ Visa® Card can take advantage of a whopping 21 months of interest-free financing on new purchases and balance transfers with no annual fee.

While this card is a tremendous offering if you need to make a large purchase or pay off existing high-APR debt on another card, the lack of rewards and slightly high APR after the introductory period might not make this the best long-term solution for your wallet.

- 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers, a variable APR thereafter. Balance transfers made within 120 days from account opening qualify for the introductory rate.

- $0 Annual Fee

- Get up to $600 of cell phone protection when you pay your monthly cell phone bill with your eligible Wells Fargo card (subject to a $25 deductible).

- Through My Wells Fargo Deals, you can have access to personalized deals from a variety of merchants. Activate your deals, then shop, dine, or enjoy an experience using an eligible Wells Fargo credit card.

- Zero liability protection plus Roadside Dispatch®

Additional Disclosure: The information related to this card has been collected by CardRates and has not been reviewed by the issuer of this product.

The Wells Fargo Reflect® Card card exceeds 18 months and offers 21 full months of 0% interest on both purchases and transfers — a truly great deal. You also get 120 days to make your transfer to take advantage of the promotional rate, which is longer than the typical 90 days.

The downsides? This card doesn’t offer any purchase rewards and it charges a balance transfer fee that is a percentage of the amount you transfer. Still, most people come out ahead when choosing to transfer a balance, as long as they can pay it off before the promotion expires.

Three Cards with No Interest on Balance Transfers for 18+ Months

A 0% balance transfer offer is good for anyone who has a large amount of debt on a credit card with a high APR. Balance transfers work by allowing you to transfer your existing debt to the new card with the added benefit of 0% interest financing, so you’re no longer being charged interest fees for the duration of the promotional period.

These cards offer a minimum of 18 months to pay your transferred balance down before the regular APR kicks in.

- 0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

- No Annual Fee - our low intro rates and all the benefits don't come with a yearly charge.

- Buy now and pay later. Split your payment for eligible purchases of $75 or more into a fixed payment with Citi® Flex Pay.

- Get free access to your FICO® Score online.

Additional Disclosure: Citi is a CardRates advertiser.

The Citi® Diamond Preferred® Card gives new cardholders interest-free financing and special access to purchase tickets for thousands of events through Citi Entertainment®. If you’re looking for a good introductory rate, this card has your back. But after that intro period ends, be prepared to pay the regular purchase APR.

- INTRO OFFER: Unlimited Cashback Match for all new cardmembers. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards.

- Earn 2% cash back at Gas Stations and Restaurants on up to $1,000 in combined purchases each quarter, automatically. You’ll still earn unlimited 1% cash back on all other purchases.

- Get a 0% intro APR for 18 months on balance transfers. Then 17.49% to 26.49% Standard Variable APR applies, based on credit worthiness.

- Redeem cash back for any amount

- No annual fee.

- Terms and conditions apply.

If you’re looking to transfer a high balance, then the Discover it® Chrome card may be for you. With this card, you could also save money on interest for purchases during its promotional period. Discover is regularly lauded for its highly rated, U.S.-based customer service team.

- Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

- Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 17.49% - 27.49%, based on your creditworthiness.

- Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

- If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Additional Disclosure: Citi is a CardRates advertiser.

The only thing better than earning cash back is earning double cash back, and the Citi Double Cash® Card gives you just that with 1% back on all purchases plus another 1% when you pay. New cardholders also receive introductory 0% financing on balance transfers, but a hefty balance transfer fee applies, and there’s no intro 0% promotional period on new purchases.

What Does 0% APR for 18 Months Mean?

Your annual percentage rate (or APR) is the annual rate charged by your credit card issuer for the convenience of borrowing money. Credit cards express an APR as a percentage that represents the actual annual cost of credit over the time it takes you to repay the debt.

So, if your APR is 21%, you’ll incur a fee of 21% of your balance annually. However, since banks usually charge interest monthly, that 21% is spread out over 12 months.

In the case of a 21% APR, you’d be charged 1.75% of your existing balance at the end of each billing cycle. Higher balances always mean greater charges.

Those interest charges are a major reason why just sticking to your minimum monthly payment can backfire. Usually, your payment barely touches the principal, making it tough to reduce your overall debt. So, relying solely on the minimum payment isn’t doing you any favors in the long term.

When you grab a 0% introductory offer from a credit card company, you don’t have to worry about interest charges during that initial period.

Some cards include transferred balances and new purchases in their introductory offer. That means you can transfer balances from an existing high-interest credit card and pay it off over the intro period without paying any of the interest charges you would have on the other card.

This method lets you pay off your debt more quickly and at a lower cost—both things we all appreciate. Just be sure to keep an eye out for any balance transfer fees when you’re moving your balance.

What are the Best 0% Interest Credit Cards?

We all have different opinions on what makes a credit card the “best.” The ideal choice for you truly hinges on your personal needs and preferences.

But no matter what you want from your new credit card, the top 0% APR offerings will all include an equal number of months in the introductory rate for balance transfers and new purchases alike. There should also be some sort of rewards structure to thank you for your business, unless you can find a balance transfer offer that doesn’t charge a balance transfer fee instead.

No credit cards currently offer 0% financing for as long as 18 months that do not charge a balance transfer fee; however, you can find card offers with shorter 0% periods without this fee.

In addition to the card’s perks, a great credit card shouldn’t hit you with high membership fees. After all, why save money during the introductory period if it’s just going to be eaten up by an annual fee?

Which Credit Card Has the Longest Interest-Free Period?

This will largely depend on your intentions for the card. That’s because some cards offer longer intro periods for balance transfers than for new purchases and vice versa.

Also, remember that card issuers frequently change terms and rates—so what’s great today might not be so appealing six months down the line. Some cards come with strings attached.

Take, for example, the U.S. Bank Shield™ Visa® Card. Current new cardholders can take advantage of an introductory 0% APR on balance transfers for a typically unheard-of length of time.

You might come across other cards offering 18 months or more of interest-free balances, but they could include an annual fee or balance transfer fee that reduces your savings. Plus, some cards might cut your interest-free period short if you happen to make a late payment.

Before you pick the card you want to apply for, make sure it aligns with all your needs. You can only take advantage of an introductory rate if you understand the terms. This might mean completing all your balance transfers within a 60-day window after opening your account or possibly paying a balance transfer fee.

Do No-Interest Credit Cards Hurt Your Credit?

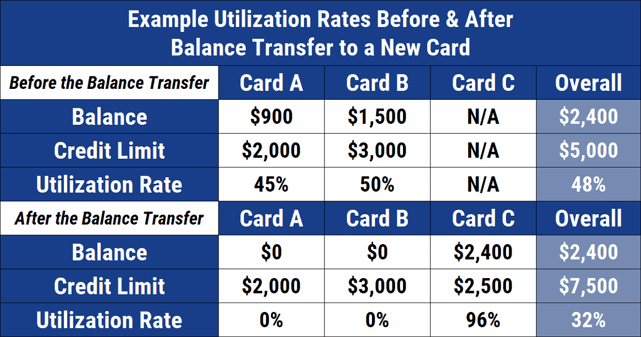

That depends on how you use the card. One of the five factors that determine your credit score — and 30% of your overall score calculation — is your credit utilization or amounts owed. You can find your current utilization by dividing your balances across cards by your total credit limits combined.

Banks usually express utilization as a percentage. For instance, if you have a credit card with a $1,000 limit and you’re carrying a balance of $250, that means you’re using up 25% of your available credit.

Credit card issuers and lenders aren’t fans of high utilization. They prefer borrowers who repay quickly and avoid those who might be overwhelmed with debt. To keep things running smoothly, try to maintain your overall utilization below 30%.

By seizing interest-free offers from credit card issuers, you can repay your debt faster while cutting down on your utilization. This way, you don’t have to worry about the high interest charges that often show up on your monthly statements. Plus, clearing your debt can give your credit score a significant lift.

But if you continue to charge on the card from which you transferred the original debt, your utilization will only increase and hurt your credit score. It could also hurt your credit score if you open a new 0% APR card to finance a big-ticket purchase that utilizes most of your available credit limit.

Keep in mind that each 0% interest credit card offer comes with its own set of terms. Some cards might begin applying interest to your remaining balance right after the introductory period ends.

Some cards might hit you with deferred interest—meaning you’ll owe interest on the total amount charged or transferred—if you don’t pay off the balance completely by the end of the introductory period.

If you end up with additional charges, your balance might quickly balloon, potentially affecting your credit score due to higher utilization. The smartest way to manage interest-free credit cards is to pay off the balance before the regular APR kicks in.

You can then evaluate whether the card still has benefits worth reserving a spot in your wallet.

Pay Your Full Balance to Avoid Ever Paying Interest

They say the best things in life are free. But when it comes to things you want or need that do cost money, why not make the most of credit card introductory offers that give you interest-free financing?

No matter what you need to pay off — be it a new purchase or existing debt — the right credit card can save you thousands in interest charges. That’s money you can put into savings or use toward life’s next big necessity.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

![Best Credit Cards with No Interest for 12+ Months[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2019/05/Best-Credit-Cards-with-No-Interest-for-12-Months-Feat.jpg?width=158&height=120&fit=crop "Best Credit Cards with No Interest for 12+ Months[updated_month_year before=\" (\" after=\")\"]")

![0% For 21 Months: Balance Transfer Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2023/04/0-Percent-Blance-Transfer-For-21-Months-Credit-Cards.png?width=158&height=120&fit=crop "0% For 21 Months: Balance Transfer Cards[updated_month_year before=\" (\" after=\")\"]")

![0% For 24 Months Balance Transfer Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2023/08/0-Percent-For-24-Months-Balance-Transfer-Cards.jpg?width=158&height=120&fit=crop "0% For 24 Months Balance Transfer Cards[updated_month_year before=\" (\" after=\")\"]")

![0% For 12+ Months: Balance Transfer Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2023/08/0-percent-for-12-months-balance-transfer-cards.jpg?width=158&height=120&fit=crop "0% For 12+ Months: Balance Transfer Cards[updated_month_year before=\" (\" after=\")\"]")

![5 Best 0% Balance Transfers For 18+ Months[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2021/05/Best-0-Balance-Transfers-For-18-Months.jpg?width=158&height=120&fit=crop "5 Best 0% Balance Transfers For 18+ Months[updated_month_year before=\" (\" after=\")\"]")

![15 Best Low-Interest Credit Cards with 0% Intro Offers[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/07/low-interest.png?width=158&height=120&fit=crop "15 Best Low-Interest Credit Cards with 0% Intro Offers[updated_month_year before=\" (\" after=\")\"]")

![15 Cheap Credit Cards: Low Interest & $0 Fees[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/12/cheap.png?width=158&height=120&fit=crop "15 Cheap Credit Cards: Low Interest & $0 Fees[updated_month_year before=\" (\" after=\")\"]")

![7 Best 0% APR & Low-Interest Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/04/low.png?width=158&height=120&fit=crop "7 Best 0% APR & Low-Interest Credit Cards[updated_month_year before=\" (\" after=\")\"]")