Writer: Eric Bank

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

Continental Finance Company sponsors the Cerulean Credit Card, an unsecured credit card for consumers with bad credit. The card offers a mix of costs and benefits that make it a good choice for folks who’ve had trouble establishing a decent credit line.

But before applying, check out our list of worthwhile alternatives that may provide you more value for your money.

-

Navigate This Article:

All About the Cerulean Credit Card

Consumers with FICO scores below 580 are the target audience for the Cerulean Credit Card. It is an unsecured Mastercard, so you don’t have to plunk down cash collateral to acquire the card.

It is neither the best nor the worst choice for subprime consumers, but you owe it to yourself to check out Cerulean’s competitors before deciding which card to get.

– How It Works

You can use the Cerulean Mastercard for purchases up to your credit limit and stretch low monthly payments over multiple billing cycles.

The card provides a 25-day grace period that starts from the end of each billing period and allows you to avoid paying interest if you pay your entire balance by the due date. If you carried a balance coming into the most recent billing period, you must pay it off in full before the grace period will resume.

The card allows cash advance transactions starting 95 days after account opening. The transaction fee is the greater of $5 or 5%. The Cerulean Mastercard doesn’t offer balance transfers.

– Rewards and Benefits

Cerulean Mastercard does not offer rewards for purchases or signup bonuses. Nor does it provide any 0% introductory APR promotions for purchases.

The card’s most significant benefit is its credit limit policy. You can establish an initial line of credit between $300 and $1,000 that you can double by paying your bill on time for six consecutive months following issuance.

Otherwise, the benefits are meager. You receive Mastercard’s standard $0 fraud liability coverage.

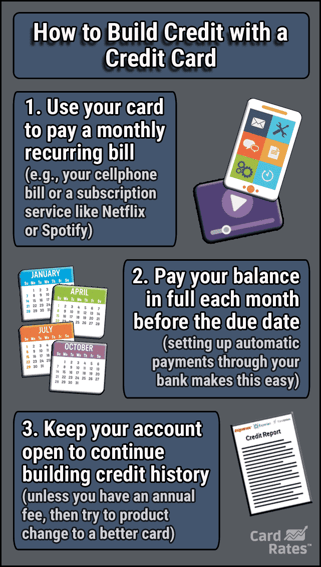

And the credit card issuer, the Bank of Missouri, reports your payments to all three major credit bureaus (TransUnion, Experian, Equifax), which can help you build credit.

Each credit bureau publishes credit reports that detail your financial accounts. Unlike traditional credit card issuers, the Bank of Missouri only issues subprime credit cards.

You also get a free monthly credit score when you enroll in electronic statements, but the type of score you receive (FICO or VantageScore) is unclear.

You can manage the card through online account access or its accompanying mobile app. The card’s website features an informative knowledge base of credit-related articles.

– APRs and Fees

The Cerulean Mastercard’s variable APR and other terms can be found here. It charges an annual fee, a foreign transaction fee, and fees for returned or late payments. You can add an authorized user for a one-time additional card fee.

– How to Get One

Continental Finance must preselect you via a mailed offer before you can apply for the Cerulean Mastercard Credit Card, which you can do:

- Via online account access at the Cerulean Credit Card login page

- By returning your acceptance certificate in the mail

- By calling Customer Service at (866) 513-4598

You seldom see invitation-only applications from traditional credit card issuers, but this issuer has no problem requiring invitations for Cerulean credit cards.

You’ll need to supply the number on your acceptance certificate when you submit your application. Required data includes your name, address, date of birth, and Social Security number.

The credit card issuer does a hard credit pull that may lower your score by a few points and remain in your credit history (on your credit report) for two years. You should get an immediate approval decision, but some applications may take up to 30 days if additional information is required.

Once approved, you should receive your new card within three business days.

You can pay your card online or by check. The credit card payment address is:

Cerulean Card

P.O. Box 6812

Carol Stream, IL 60197-6812

While you could send a check to the credit card payment address, online payments are processed much faster.

Best Cerulean Credit Card Alternatives

Here are some more unsecured credit cards for bad credit you can consider. You can get these without an invitation, and some may offer features you won’t find on Cerulean credit cards.

- Up to $1,000 Initial Credit Limit

- See if you Pre-Qualify with No Impact to your Credit Score

- Less than perfect credit? We understand. The Surge Mastercard is ideal for people looking to rebuild their credit.

- Unsecured credit card requires No Security Deposit

- Perfect card for everyday purchases and unexpected expenses

- Monthly reporting to the three major credit bureaus

- Use your card everywhere Mastercard is accepted at millions of locations

- Enjoy peace of mind with Mastercard Zero Liability Protection for unauthorized purchases (subject to Mastercard guidelines)

- Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

Surge® Platinum Mastercard® from Continental Finance provides Mastercard Zero Liability Protection to guard you against charges you didn’t make. The accompanying mobile app lets you pay bills, view statements, specify direct deposits, and check payment due dates. Its purchase APR is below that of some competitors, and the card doesn’t punish late payments with a penalty APR.

- Up to $1,000 Initial Credit Limit

- See if you Pre-Qualify with No Impact to your Credit Score

- Less than perfect credit? We understand. The Reflex Mastercard is ideal for people looking to rebuild their credit.

- Unsecured credit card requires No Security Deposit

- Perfect card for everyday purchases and unexpected expenses

- Monthly reporting to the three major credit bureaus

- Use your card everywhere Mastercard is accepted at millions of locations

- Enjoy peace of mind with Mastercard Zero Liability Protection for unauthorized purchases (subject to Mastercard guidelines)

- Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

Reflex® Platinum Mastercard®, also from Continental Finance, is a carbon copy of the Surge Mastercard®. It doesn’t impose a monthly maintenance fee for the first year and offers Mastercard fraud protection.

- Guaranteed $700 credit limit if approved.

- Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

- Don’t Have Perfect Credit? No Problem!

- Join over a million consumers who are working on building their access to credit.

- Zero Fraud Liability – Peace of mind that comes with having a Mastercard.

- Get the credit you deserve, even with less-than-perfect history.

- No security deposit, and a path to better credit.

Milestone® Mastercard® targets consumers who don’t have good credit. It takes only a minute to apply, and the card issuer may recommend other cards to consider if it rejects your current application. This unsecured credit card does not charge a monthly maintenance fee for the first year and offers mobile access.

Best Alternatives If You Don’t Qualify For an Unsecured Card

These secured credit cards deserve your strong consideration if you don’t have good credit. They collect a security deposit upfront, but the deposit money — unlike fees — is refundable. These secured cards have better terms and conditions than similar unsecured cards, and some even offer cash back rewards.

- No annual or hidden fees, and you can earn unlimited 1.5% cash back on every purchase, every day. See if you’re approved in seconds

- Put down a refundable $200 security deposit to get at least a $200 initial credit line

- Building your credit? Using a card like this responsibly could help

- Enjoy peace of mind with $0 Fraud Liability so that you won’t be responsible for unauthorized charges

- You could earn back your security deposit as a statement credit when you use your card responsibly, like making payments on time

- Be automatically considered for a higher credit line in as little as 6 months with no additional deposit needed

- Earn unlimited 5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

- Monitor your credit score with CreditWise from Capital One. It’s free for everyone

- Top rated mobile app

The may be the best secured credit card for rebuilding credit. It provides unlimited cash back rewards on all eligible purchases without charging an annual or foreign transaction fee. You can earn a credit limit increase or card upgrade by consistently paying your bills on time.

- No annual or hidden fees. See if you’re approved in seconds

- Building your credit? Using the Capital One Platinum Secured card responsibly could help

- Put down a refundable security deposit starting at $49 to get at least a $200 initial credit line

- You could earn back your security deposit as a statement credit when you use your card responsibly, like making payments on time

- Be automatically considered for a higher credit line in as little as 6 months with no additional deposit needed

- Enjoy peace of mind with $0 Fraud Liability so that you won’t be responsible for unauthorized charges

- Monitor your credit score with CreditWise from Capital One. It’s free for everyone

- Get access to your account 24 hours a day, 7 days a week with online banking to access your account from your desktop or smartphone, with Capital One’s mobile app

- Top rated mobile app

You may be eligible for the Capital One Platinum Secured Credit Card even if your credit is awful. The $200 initial credit line may be available for a deposit of as low as $49, a unique feature of this card. The card issuer may grant you a credit limit increase if you consistently pay your bills on time.

- No minimum balance requirements*

- No credit check**

- 2% cash back on category of choice with direct deposit***

- The perks of credit building meet the best of banking****

- Chime Checking Account required to apply for the Chime Visa® Credit Card

Chime is a financial technology company, not a bank. Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC. The secured Chime Visa® Credit Card is issued by The Bancorp Bank, N.A. or Stride Bank, N.A. pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa credit cards are accepted. Please see the back of your Card for its issuing bank.

*Money added to Chime CardTM will be held in a secured deposit account as collateral for your Chime Card, and you can spend up to this amount. You can use money deposited in your Secured Deposit Account to pay off your charges at the end of every month.

**Out-of-network ATM withdrawal and over the counter advance fees may apply.

***With a qualifying direct deposit, earn 2% cash back on category of choice on eligible secured Chime Visa® Credit Card purchases.

****On-time payment history may have a positive impact on your credit score. Late payment may negatively impact your credit score. Results may vary.

The The secured Chime Visa® Credit Card is a great credit card option for folks with bad or limited credit. The card rewards you with cash back on eligible purchases and has no annual fees. With this card, you won’t need a credit check to get approved, and there isn’t a minimum balance requirement.

7. Citi® Secured Mastercard®

This card is currently not available.

Additional Disclosure: The information related to Citi® Secured Mastercard® has been collected by CardRates.com and has not been reviewed or provided by the issuer or provider of this product or service.

The Citi® Secured Mastercard® can build credit when you have no, limited, or poor credit. The card doesn’t provide rewards like some comparable secured cards but is still a good option for improving your credit score through responsible use.

Is Cerulean a Real Credit Card?

Yes, Cerulean Mastercard Credit Card is genuine and can help you rebuild your credit without demanding a security deposit. Its credit-building features include payment reporting to all three major credit bureaus and free monthly credit scores from one credit bureau.

You can double your credit line in only six months, and the card allows you to make cash advance transactions.

Less advantageous are the card’s steep annual fee and murky application process. You can’t access the Cerulean Credit Card login unless you receive an invite.

The marketing strategy behind invitation-only applications isn’t clear, but Continental Finance Company must think it is a practical approach. We’d like to see lower costs and the addition of rewards or introductory promotions.

Which Type of Credit Card Is Better For Bad Credit — Secured or Unsecured?

We vote for secured cards. Here’s why:

- Easier to get: It’s generally much easier for subprime consumers to qualify for a secured card. The security deposit makes all the difference. Amazingly, some secured cards don’t even check your credit. You will own a working credit card that happens to be secured — without any outward hint to the rest of the world.

- Best of both worlds: Most secured credit cards will upgrade you to an unsecured version if you pay your bills on time over a set period. That means you’ll have your deposit returned and own an unsecured card despite your bad credit score.

- Lower costs: Secured cards don’t charge signup or maintenance fees. They have no or low annual fees, and their APRs are usually several percentage points lower than the rates similar unsecured cards charge.

- Better perks: You can get a secured card that pays rewards. That’s unheard-of among subprime unsecured cards. You may also get other benefits, such as rental car collision damage waiver or cellphone insurance.

Remember, security deposits are refundable, but fees are not. In the long run, secured credit cards are the better choice for folks with credit problems.

Which Card Is the Closest Alternative to the Cerulean Credit Card?

Surge® Platinum Mastercard®, which is also from Continental Finance, is very similar to the Cerulean Mastercard. It has a similar credit limit potential, and the costs are about the same.

- Up to $1,000 Initial Credit Limit

- See if you Pre-Qualify with No Impact to your Credit Score

- Less than perfect credit? We understand. The Surge Mastercard is ideal for people looking to rebuild their credit.

- Unsecured credit card requires No Security Deposit

- Perfect card for everyday purchases and unexpected expenses

- Monthly reporting to the three major credit bureaus

- Use your card everywhere Mastercard is accepted at millions of locations

- Enjoy peace of mind with Mastercard Zero Liability Protection for unauthorized purchases (subject to Mastercard guidelines)

- Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

We assume that their Customer Service operations are similar since Continental Finance sponsors both cards. The most significant difference between the two cards is their availability. You need an invitation to get the Cerulean card, but not the Surge credit card.

We don’t see why anyone would wait for an invitation to a subprime card, which makes the Surge credit card a better choice for most consumers with bad credit.

Subprime Consumers Have Many Credit Card Options

CardRates.com has reviewed more than two dozen credit cards for bad credit, including the ones in this article. You undoubtedly have a wide array of credit card choices despite your low credit score, so you should look for the card offer that best matches your needs.

The Cerulean Mastercard deserves consideration if you receive an invitation, but it’s hardly worth the wait. You can get more information about the readily available credit cards reviewed above by clicking on the APPLY HERE links above.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![Surge Credit Card: Review & 5 Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2016/11/surgecard.jpg?width=158&height=120&fit=crop "Surge Credit Card: Review & 5 Alternatives[updated_month_year before=\" (\" after=\")\"]")

![Mercury Credit Card: Review & 5 Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/05/Mercury-Credit-Card-Review.jpg?width=158&height=120&fit=crop "Mercury Credit Card: Review & 5 Alternatives[updated_month_year before=\" (\" after=\")\"]")

![Instacart Credit Card: Review & 5 Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/09/Instacart-Credit-Card.jpg?width=158&height=120&fit=crop "Instacart Credit Card: Review & 5 Alternatives[updated_month_year before=\" (\" after=\")\"]")

![[card_field card_choice='16924' field_choice='title' link_type='none'] Review & Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/06/Surge-Mastercard-Reviews.jpg?width=158&height=120&fit=crop "[card_field card_choice='16924' field_choice='title' link_type='none'] Review & Alternatives[updated_month_year before=\" (\" after=\")\"]")

![[card_field card_choice='31445' field_choice='title']: Review & Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/03/preferred.png?width=158&height=120&fit=crop "[card_field card_choice='31445' field_choice='title']: Review & Alternatives[updated_month_year before=\" (\" after=\")\"]")

![Chase’s [card_field card_choice='39321' field_choice='title']: Review & Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/03/inkcash.png?width=158&height=120&fit=crop "Chase’s [card_field card_choice='39321' field_choice='title']: Review & Alternatives[updated_month_year before=\" (\" after=\")\"]")

![Walmart MoneyCard: Review & Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/03/Walmart-MoneyCard-Review.jpg?width=158&height=120&fit=crop "Walmart MoneyCard: Review & Alternatives[updated_month_year before=\" (\" after=\")\"]")

![[card_field card_choice='68438' field_choice='title' link_type='none'] Review & Alternatives[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/03/Citi-Secured-Credit-Card-Review.jpg?width=158&height=120&fit=crop "[card_field card_choice='68438' field_choice='title' link_type='none'] Review & Alternatives[updated_month_year before=\" (\" after=\")\"]")