Writer: Adam West

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

American consumers have taken on a growing amount of credit card debt in the years since the Great Recession. Many who see this trend as unsustainable are looking to consolidate credit cards onto one card in an effort to reduce the total debt they carry, not to mention the amount they pay each year in interest.

A recent study found consumers have an average of four credit cards with a combined balance of nearly $6,200, which costs an average of $1,162 annually in interest. If you’re one of the millions of consumers with a mountain of debt spread across multiple cards, consolidating that debt into a single payment probably sounds pretty good.

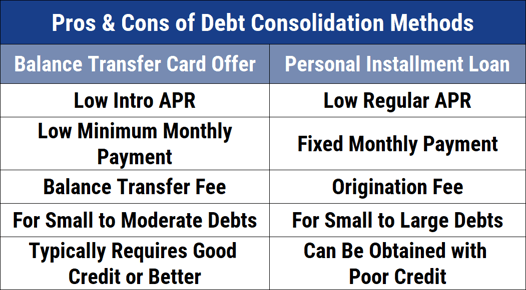

Among the ways to consolidate credit card debt are using balance transfer credit cards and debt consolidation loans. However, of your available choices, the easiest and most effective way is to transfer your card balances to a single card with a low or even 0% interest rate.

Balance Transfer Cards | Loan Consolidation | FAQs

A Balance Transfer is the Best Way to Consolidate Debt

It may seem counterintuitive but getting another credit card might be the best way to pay off credit card debt. Of course, it must be the right card, one that’s specifically designed for transferring the balances from other high-interest credit cards.

Balance transfer credit cards usually have an introductory interest rate period, many at 0% APR, that lasts for as long as 18 months. Here are our selections for the best balance transfer cards to consolidate credit card debt.

- New! 0% Intro APR for 21 billing cycles for purchases, and for any balance transfers made in the first 60 days. After the Intro APR offer ends, a Variable APR that’s currently 14.99% - 25.99% will apply. A 5% fee applies to all balance transfers. Balance transfers may not be used to pay any account provided by Bank of America.

- No annual fee.

- No penalty APR. Paying late won't automatically raise your interest rate (APR). Other account pricing and terms apply.

- This offer may not be available elsewhere if you leave this page. You can take advantage of this offer when you apply now.

- 0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

- No Annual Fee - our low intro rates and all the benefits don't come with a yearly charge.

- Buy now and pay later. Split your payment for eligible purchases of $75 or more into a fixed payment with Citi® Flex Pay.

- Get free access to your FICO® Score online.

Additional Disclosure: Citi is a CardRates advertiser.

- New! 0% Intro APR for 21 billing cycles for purchases, and for any balance transfers made in the first 60 days. After the Intro APR offer ends, a Variable APR that’s currently 14.99% - 25.99% will apply. A 5% fee applies to all balance transfers. Balance transfers may not be used to pay any account provided by Bank of America.

- No annual fee.

- No penalty APR. Paying late won't automatically raise your interest rate (APR). Other account pricing and terms apply.

- When handled responsibly, a credit card can help you build your credit history, which could be helpful when looking for an apartment, a car loan, and even a job.

- This offer may not be available elsewhere if you leave this page. You can take advantage of this offer when you apply now.

- INTRO OFFER: Unlimited Cashback Match for all new cardmembers. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards.

- Earn 2% cash back at Gas Stations and Restaurants on up to $1,000 in combined purchases each quarter, automatically. You'll still earn unlimited 1% cash back on all other purchases.

- Get a 0% intro APR for 18 months on balance transfers. Then 17.49% to 26.49% Standard Variable APR applies, based on credit worthiness.

- Redeem cash back for any amount

- No annual fee.

- Terms and conditions apply.

- Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

- Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 17.49% - 27.49%, based on your creditworthiness.

- Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

- If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Additional Disclosure: Citi is a CardRates advertiser.

In addition to the cards on this list, many credit unions offer balance transfer credit cards with 0% introductory rates, some of which charge no balance transfer fee. Other credit union balance transfer cards have fixed low interest rates designed for longer-term debt consolidation.

If you’re not a member already, you can check this credit union locator for the ones that serve your community.

Consolidating with a Loan is the Next Best Option

If you have too much debt to fit on a single card or if your credit score doesn’t let you qualify for a good balance transfer offer, your next best option may be a debt consolidation loan. Debt consolidation loans have the advantage of offering a fixed APR that is usually less than what a standard credit card charges.

Getting a loan to pay off high-interest credit card debt can help several ways, including reducing your monthly payments, helping you pay down debt faster, and improving your credit score by lowering your overall credit utilization rate. Here are some types of debt consolidation loans you may want to consider.

Home Equity Loans

A home equity loan lets you borrow money against the value of your home, that is assuming your home is worth more than what you owe on any mortgage you have. Of course, using a home equity loan for debt consolidation has both positive and negative aspects — some of them obvious, and others that you may not have considered.

Among the advantages of a home equity loan over a personal loan are a generally lower APR, a longer repayment period, and the potential tax deduction that can further lower the effective rate you pay. LendingTree is one such provider of home equity loans that we recommend.

- Find lenders for new home purchases, refinancing, home equity loans, and reverse mortgages

- Lenders compete for your business

- Offers in minutes

- Receive up to 5 loan offers and select the right one for you

- Founded in 1996

- Over $250 billion in closed loan transactions

On the surface, the advantages of a home equity loan may seem overwhelmingly positive, but let’s consider why they deserve a little more scrutiny.

Having more time to repay debt — in the case of a home equity loan, as much as five to 30 years — can add a lot to the total cumulative interest you pay. Be sure you don’t end up paying more interest in the long run.

For example, if you can pay off your credit card debt in two years vs. transferring it to a five-year home equity loan, the added interest cost may not be worth it.

Now for the primary and obvious disadvantage of this type of loan — the risk of losing your home if you default. Because your home is collateral for a home equity loan, failure to repay can result in forfeiture of the asset.

By comparison, defaulting on credit card debt is bad, but won’t result in you being homeless.

Personal Loans

Getting a personal loan to consolidate debt on multiple credit cards is an option to consider. But the APR on this type of loan can vary greatly depending on the lender. The rate you’ll pay is also directly tied to your credit score, the type of lender you choose, and the length of the loan.

Personal loans, also called signature loans, require no collateral. Because of this, interest rates on these loans can vary widely.

The following lending networks may approve you for a loan large enough to pay off your credit card debt at a lower interest rate than what you’re currently being charged.

- Loans from $500 to $10,000

- All credit types accepted

- Receive a loan decision in minutes

- Get funds directly to your bank account

- Use the loan for any purpose

- Loan amounts range from $500 to $10,000

- Compare quotes from a network of lenders

- Flexible credit requirements

- Easy online application & 5-minute approval

- Funding in as few as 24 hours

- Loan amounts range from $1,000 to $35,000

- All credit types welcome to apply

- Lending partners in all 50 states

- Loans can be used for any purpose

- Fast online approval

- Funding in as few as 24 hours

Banks and credit unions tend to offer the lowest rates, but they also have the strictest loan qualification requirements. Online lenders and lender networks offer a wider variety of loans for different credit types but may charge higher interest rates.

According to the Federal Reserve Bank of St. Louis, the average finance rate for a 24-month personal loan at a commercial bank is just over 10%. That compares with an average credit card interest rate in the U.S. north of 15%. So, providing you have good to excellent credit, a personal loan can save you quite a bit in interest charges.

But what if your credit isn’t among the top tier? How much can you expect to pay for a personal loan if you have to look outside the traditional bank lending environment?

Online lenders can charge rates of up to 35.99% for those with bad credit, but the average APR you can expect will likely be near or slightly less than that of a credit card.

401(k) Loans

If you currently participate in a 401(k) employer-sponsored retirement plan, you may be able to borrow from your account to consolidate and pay off debt. However, just because this is an option, doesn’t mean it’s the best choice for a loan.

If you make the decision to borrow from your 401(k), you must be aware of the plan’s many rules and restrictions. Borrowing even a small amount from your 401(k) can greatly reduce what you’ll have available for use in retirement.

First, the amount you are legally able to borrow can’t exceed 50% of your total vested account, up to a maximum of $50,000. Also, the loan must be repaid through payroll deductions over a maximum of five years.

There are also restrictions and caveats that involve eligibility, such as if you leave your job or want to transfer your 401(k) to an IRA. This can mean you must repay the loan in full or pay an early withdrawal penalty.

The argument in favor of taking out a 401(k) loan is that the interest rate is often very low. The interest rate calculation varies by plan administrator but tends to be something just above the Prime Rate.

Also, whatever interest you pay goes directly back into your account, helping to offset some of the compound gains you’re losing by withdrawing funds.

Can I Consolidate Credit Card Debt onto One Card?

If you’re carrying a balance on multiple credit cards, it’s a good bet you’re paying more in interest than you need to. You can save a bundle by transferring those balances onto a single card with a low or even zero interest rate.

But can you really consolidate all of that debt onto a single card? In a word, yes.

Credit card offers with 0% interest rates on balance transfers are designed to help you consolidate debt from multiple cards. However, you need to ask some questions when deciding whether to go this route:

- How much total debt will I be consolidating, and will the credit limit of the new card cover it? Depending on factors like your credit utilization ratio, credit score, and the number of cards you have, the credit limit you receive may not allow you to transfer all of your debt to the new card. In this case, choose the balances with the highest interest rates to consolidate first.

- How long is the introductory rate period? Most 0% introductory offers are good for at least 12 months, and some extend as long as 21 months. Be sure you know the terms of the card you’re applying for. Also, pay attention to the rate you will pay after the intro period, as some of them charge a very high standard APR.

- Is there a balance transfer fee, and how will it impact what I pay? Most balance transfer cards charge a one-time 3% fee to transfer a balance. That means $30 for every $1,000 you transfer. Be sure to include this fee when calculating whether this is the right choice for you.

Consolidating the balance from multiple credit cards onto a single card can be a good financial choice, as long as it’s done the right way. Be sure you can pay off the transferred balance within the introductory rate period.

Also, carefully consider the details of the card you plan to get and shop around for the longest intro-rate period and lowest balance transfer fees you can find.

Is Consolidating Credit Card Debt Bad for Your Credit?

Taking charge of your financial life by consolidating credit card debt is seldom a bad thing. But the method you use can have a big impact on your credit score.

One way your score can take a hit depends on what you do after being approved for a balance transfer card. When you consolidate existing credit card debt onto a new balance transfer card, don’t cancel your old credit cards.

Doing so can have the effect of driving up your credit utilization rate, which accounts for 30% of your FICO score. This rate is calculated by dividing your overall credit card balance by the available credit you have. Closing your old cards will lower your available credit.

Another way your credit score could potentially be hurt involves an unintended consequence of debt consolidation. If you transfer high-interest balances to a new low-interest card, it may feel like a fresh start.

All of those cards that now have a zero balance may start begging to be used… don’t do it! Debt consolidation only works if it’s part of a plan to curb spending and actually pay down the amount you owe.

The benefits to your credit score when consolidating credit card debt the right way far outweigh any potential harm. By paying off cards, reducing your overall debt, and actively monitoring your spending, you’ll likely find your credit score increasing rather than dropping.

What is the Smartest Way to Consolidate Debt?

At the risk of sounding simplistic, the smartest way to consolidate credit card or any debt is the way that works best for you.

For some, that could mean getting a balance transfer card with a high enough credit limit and a long introductory rate period. For others, a debt consolidation loan might be the best choice. Whichever route you decide is best, having a plan and executing it is crucial.

Consider the amount you owe, the amount you’re paying in interest on what you owe, and the amount you can pay each month toward the balance of what you owe. Any choice you make for a credit card or loan to consolidate your debt should be based on these three factors.

Remember that consolidating and beginning to pay down your debt is just the first step — you also need to take control of your spending. It makes no sense to reduce your debt at the same time you are taking on more. Make a budget and stick to it.

Debt consolidation, whether done with a balance transfer credit card, a low-interest personal loan, a home equity or other type of loan, should be seen as a means to an end. The ultimate goal is to reduce your debt and the amount you’re paying in interest.

Prepare for What’s Next

American consumers have taken on an increasing amount of debt in the years following the economic recovery. However, consumer debt can’t continue to grow unrestrained.

For those who see credit card debt as an unnecessary drain on their hard-earned resources, consider paying off debt by consolidating onto a single low-interest credit card or loan. It’s one of the best ways to ensure you’re prepared for whatever the economy brings.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

![8 Best Cards to Consolidate Credit Card Debt[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/08/consolidatecard3.png?width=158&height=120&fit=crop "8 Best Cards to Consolidate Credit Card Debt[updated_month_year before=\" (\" after=\")\"]")

![How to Consolidate Credit Card Debt[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/01/consolidate.png?width=158&height=120&fit=crop "How to Consolidate Credit Card Debt[updated_month_year before=\" (\" after=\")\"]")

![Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/06/Can-I-Use-My-Credit-Card-Before-Closing-on-a-Home.jpg?width=158&height=120&fit=crop "Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=\" (\" after=\")\"]")

![List of Subprime Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/10/list.jpg?width=158&height=120&fit=crop "List of Subprime Credit Cards[updated_month_year before=\" (\" after=\")\"]")

![Can You Pay a Credit Card with a Credit Card? 3 Ways Explained[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/02/card-with-card-2.png?width=158&height=120&fit=crop "Can You Pay a Credit Card with a Credit Card? 3 Ways Explained[updated_month_year before=\" (\" after=\")\"]")

![[updated_month_year after=" "]Cash Advance Limits by Issuer[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2020/12/shutterstock_2980733.jpg?width=158&height=120&fit=crop "[updated_month_year after=\" \"]Cash Advance Limits by Issuer[updated_month_year before=\" (\" after=\")\"]")

![11 Best Credit Cards for Consolidation[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/06/consol.png?width=158&height=120&fit=crop "11 Best Credit Cards for Consolidation[updated_month_year before=\" (\" after=\")\"]")

![11 Best Credit Cards to Pay Off Debt[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2019/06/Best-Credit-Cards-to-Pay-Off-Debt-Feat.png?width=158&height=120&fit=crop "11 Best Credit Cards to Pay Off Debt[updated_month_year before=\" (\" after=\")\"]")