Writer: Mike Senecal

Editor: Jon McDonald

Reviewer: Ashley Fricker

Opinions expressed here are ours alone, and are not provided, endorsed, or approved by any issuer. Our articles follow strict editorial guidelines and are updated regularly.

If you run up credit card debt, you have to make monthly payments until you repay it all. If you stop paying, you’ll enter default status.

Credit card default is when issuers determine you will no longer repay your account, which is typically after 180 days or about six months. Trust me — you want to deal with your obligation before it reaches that point.

A credit card issuer will typically default your account if you don’t make payments for 180 days.

Not making payments also damages your credit score, limits your future financial prospects, and could even land you in court. Nobody wants that.

I wrote this guide to detail the causes of default, offer guidance to keep you out of trouble, and explain the steps you can take to recover. A credit card default can be life-changing, but it’s also preventable. Read on to learn how to avoid it.

-

Navigate This Article:

Basics of Credit Card Default

Understanding the basic concepts and implications of defaulting on a credit card is pretty straightforward, but the devil is in the details.

Here, I’ll walk you through the timeline and the steps card issuers take when they stop receiving monthly payments, how that information damages credit scores, and when and why the law occasionally steps in.

Credit Card Default Timeline

You’re officially late the moment you pass your due date without your card issuer receiving payment. The good news is that you don’t suddenly transition from a missed payment deadline to a default status.

Card companies generally consider accounts past due as delinquent or seriously delinquent before transitioning them to default status after 180 days.

But time flies if you’re unaware. A typical timeline breakdown of what you can expect when your card company stops receiving payments looks like this:

1-29 Days Past Due: Missed Payment

Your issuer will repeatedly notify you about your lateness via email, text, or phone. You may receive a late-fee notice, but timelines and amounts vary. Crucially, issuers do not report late payments to credit bureaus at this stage.

30-59 Days Past Due: Second Missed Payment

Your card company now understands that something is seriously wrong and reports your late status to credit bureaus. In the U.S., that means reporting to the three major credit bureaus, Equifax, Experian, and TransUnion, so familiarize yourself with those names if you don’t know them already.

Credit bureaus use unique credit scoring models from companies like FICO to generate credit scores. Your second missed payment will invariably cause your score to drop.

60-89 Days Past Due: Third Missed Payment

You’re approaching a point of no return where undoing the damage becomes more difficult. Missing a third payment may prompt your issuer to increase its efforts to contact you.

You’ll also receive another ding on your credit score.

90-119 Days Past Due: Fourth Missed Payment

Another round of reports to the bureaus and hits to your credit score result in substantial damage after four missed payments.

Depending on whether you communicate with your issuer about the problem, you may receive a repayment plan proposal to avoid default or become subject to collection efforts.

120-179 Days Past Due: Final Warnings

It’s not in your issuer’s interest to see your account go into default because it constitutes a financial loss for the company. As issuers prepare for the worst, legal proceedings to collect the debt may begin as final notices of impending default go out.

180 Days Past Due: Default and Charge-Off

Issuers have usually had enough by six months past due. Your issuer will declare and charge off your account as in default, writing down the debt as a loss and reporting it to the credit bureaus.

Your issuer will also likely sell your account to a third-party collection agency, setting you up for continual contact with people who want you to repay your debt.

The debt doesn’t go away. As you’ll see in the next section, a charge-off results in significant and lasting damage to your credit score.

Consequences of Default

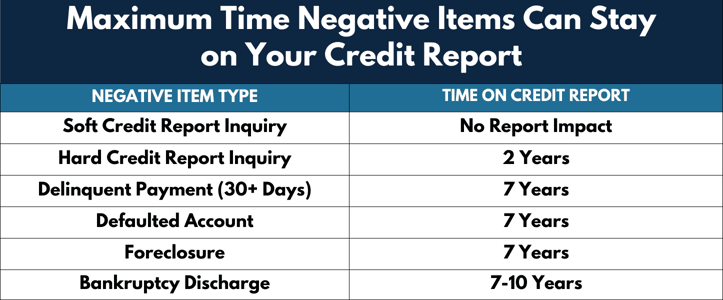

A default permanently damages your credit score for up to seven years. Getting back on track can mitigate the damage over time, but the record will remain until each bureau removes it from your credit report.

Lower credit scores caused by default or another financial mishap can increase mortgage costs, rental property access, insurance premiums, and utilities and damage employment prospects because of what they indicate about the borrower’s ability to repay.

It’s important to note that your issuer may impose additional fees and penalties after a third-party collection agency assumes your account, but it’s unlikely.

Collection agencies have separate policies regarding fees and interest that can cause your obligation to increase. Collection agencies are often open to debt settlement negotiations.

Possible Legal Ramifications

Depending on the situation, legal action from creditors attempting to recover the amount you owe — plus fees and penalties — can ensnare your finances for years.

If they feel they can make a case, collection agencies that have already hounded you for repayment through letters, phone calls, emails, and texts may file lawsuits to collect the debt.

It’s a numbers game: It’s all about calculating the relative risk of investing in litigation versus what they think they can get out of it.

Your credit card issuer may take you to court to recover what you owe or it could sell your debt to a collection agency.

Meanwhile, your original creditor — your card issuer — may pile on with additional litigation.

Collection agencies and other creditors may obtain court judgments to garnish wages through paycheck deductions, seize bank account funds, and place property liens that produce payment when the property changes owners.

The bottom line is that if you conceal your ability to repay the debt, someone in the system will eventually find out.

Common Causes of Credit Card Default

How do people put themselves into situations with such financially unproductive consequences? Many complex factors may lead to a credit card default.

People’s finances differ, and many social factors may impact a person’s approach to responsible financial management.

My intuition tells me that for every person with a record of default who dropped the ball and overspent, another did everything right but washed out in the economy or because an emergency pushed them over the financial edge.

Sudden Financial Hardship

For those latter folks, job loss, unforeseen medical expenses, and other unexpected financial misfortunes may combine with income limitations and a lack of emergency savings to create a perfect storm.

Macroeconomic changes — downturns, inflation, rising living costs, reduced purchasing power, and the like — may contribute to the problem.

Death, divorce, family changes, relocation, and other significant events may impose different but no less impactful burdens on under-resourced households.

Poor Financial Management

But let’s not discount the possibility that some with credit card defaults on their records had it coming.

Bad things happen when people spend more than they earn and prioritize more spending over paying down debt.

Consistently spending beyond your budget will result in debt that you may not be able to pay off.

Failure to budget and curb excessive lifestyle consumption can lead to a debt spiral, where there isn’t enough money coming in to recover.

Some people try to forget about the debt on their existing cards by sneaking new cards into the mix. But, as we’ve learned, the debt never goes away.

Lack of Financial Education

Of course, some default sufferers may not have the skills to manage the many inputs that make up a modern consumer lifestyle through budgeting and impulse control.

Some may not understand the impact of poor financial management on their credit scores or that credit scores even exist. They may not understand how credit score damage from financial mistakes can dog them for years.

Poor financial management can be due to a lack of financial education, but plenty of online resources exist. So, get yourself up to speed!

Credit card companies are not responsible for ensuring their customers understand credit before they grant them the right to use a financial product.

Instead, it’s a buyer-beware situation: You’ve just got to know what you’re getting into before you use a credit card or prepare to suffer the consequences!

How to Prevent Credit Card Default

I hope I haven’t discouraged you from reading further and discovering how easy it can be to manage your finances.

It’s worth it because wise credit card use can increase your cash flow, earn rewards and perks, and set you up for lasting success. Here, I’ll explain the importance of budgeting and saving to help get you there.

Budgeting and Planning

Creating and sticking to a budget is fundamental to responsible financial management. Adopting one of many popular budgeting methods can help you avoid the extra expense of late fees by keeping track of payment due dates while setting short- and long-term financial goals.

A budget will allow you to differentiate between wants and needs by limiting spending to categories you choose and setting aside cash to use instead of credit.

Make a budget and stick with to ensure you can make all of your debt repayments on time.

Putting some or all of that cash in an emergency savings fund can earn interest while silently waiting to tide you over when a flat tire or busted fridge threatens your planning.

Careful budgeting is a hallmark of financial responsibility and the best way to reduce counterproductive impulse purchases. Knowing you have a goal is great for curbing excessive spending on unneeded items.

Responsible Credit Card Use

Card companies charge you interest for the privilege of holding your debt, but they don’t receive that windfall if you pay what you owe by the due date. I can’t recommend anything more vital to using your credit cards responsibly than staying within your budget.

Keeping tabs on your spending brings all the benefits of using cards, including convenience, cash flow, rewards, and a credit score boost, without adding additional costs or threatening your financial health.

However, carrying a balance is practically inevitable for many (and an excellent reason to have a card in the first place). If you must maintain a balance, keep it as low as possible relative to your credit limit to avoid damaging your credit score through excessive credit utilization.

Contact Your Credit Card Issuer

As with many things in life, communication is the key: The best thing you can do if you have credit card trouble is to contact your issuer.

Your credit card issuer wants you to pay off your debt, so it has an incentive to work with you if you experience financial hardship.

Remember that your issuer isn’t out to get you: The last thing an issuer wants is a default. Explaining your hardship will likely win you a reprieve, such as lower interest or an invitation to negotiate a payment plan or settlement.

Your card issuer wants to work with you. Let it.

Explore Debt Relief Options

In consultation with your advisors, whoever they may be, you may also conclude that stronger measures are necessary.

Debt consolidation can combine multiple debts under one lower-interest umbrella to reduce monthly repayment expenses. Consolidation combined with budgeting can help you shed your burden and emerge in a positive financial state.

Debt settlement services are also an alternative. Choose partners carefully. If a solution sounds too good to be true, it probably is. Develop a trusted source of financial advice and make the move that is in your best interest.

That may include bankruptcy. Although declaring bankruptcy can have long-standing and profound negative financial consequences in certain situations, it can also pave the wave for a fresh start.

Never rule out bankruptcy or any other credit default solution if it comes up in conversation with someone you trust.

Don’t Let Credit Card Default Wreck Your Finances

Confidence is crucial in money management. You want to position yourself as an authority over your finances, not an unwilling participant.

Nothing is certain in finance as in life, but you’ll be fine if you understand how the system works, where you’re vulnerable, and what you can do to protect yourself from harm.

At least you will have done what you can to navigate the unpredictable waters of the credit card world. Doing what you can to avoid defaulting on credit card debt usually pays off.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![6 Great Reasons to Use a 0% APR Deal[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/05/0-APR-Deal.jpg?width=158&height=120&fit=crop "6 Great Reasons to Use a 0% APR Deal[updated_month_year before=\" (\" after=\")\"]")

![Credit Card Issuer Market Share: Top 30 Issuers[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2020/08/shutterstock_1521729479.jpg?width=158&height=120&fit=crop "Credit Card Issuer Market Share: Top 30 Issuers[updated_month_year before=\" (\" after=\")\"]")