Writer: Erica Sandberg

Editor: Ashley Fricker

Reviewer: Ashley Fricker

Disclosure: When you apply through links on our site, we may earn a referral fee from our partners. For more, see our ad disclosure and review policy.

Credit cards that offer 0% APR deals to new cardholders can be compelling. There are two basic types — one for new purchases and the other for balance transfers. Some even offer a 0% APR on new purchases and balance transfers. They work like this:

New purchases: When you open the account, you may have a year or longer to use the credit card for purchases without financing fees on any debt you carry over from month to month.

Balance transfers: You can open a credit card and move existing debt to the new card account. Although there is typically a fee to transfer a balance from another card, the issuer won’t apply financing fees to the debt you move over during the 0% APR time frame.

So if you’re looking for reasons to make the leap and apply for a 0% APR card, here are six to get you started.

1. You Are in a Temporary Financial Bind

There may come a time when you need to purchase something important, but you do not have the money to pay for it all at once. As long as you can meet the minimum payments and pay the debt off within the 0% APR time frame, charging your expense may make sense.

For example, let’s say your car broke down. The repairs cost you $3,000, which you do not have in your checking or savings account. The following cards give you more than a year to pay the debt off with no interest added.

- New! 0% Intro APR for 21 billing cycles for purchases, and for any balance transfers made in the first 60 days. After the Intro APR offer ends, a Variable APR that’s currently 14.99% – 25.99% will apply. A 5% fee applies to all balance transfers. Balance transfers may not be used to pay any account provided by Bank of America.

- No annual fee.

- No penalty APR. Paying late won’t automatically raise your interest rate (APR). Other account pricing and terms apply.

- This offer may not be available elsewhere if you leave this page. You can take advantage of this offer when you apply now.

- $200 online cash rewards bonus after you make at least $1,000 in purchases in the first 90 days of account opening.

- Earn 6% cash back for the first year in the category of your choice. You’ll automatically earn 2% cash back at grocery stores and wholesale clubs, and unlimited 1% cash back on all other purchases. After the first year from account opening, you’ll earn 3% cash back on purchases in your choice category.

- Earn 6% and 2% cash back on the first $2,500 in combined purchases each quarter in the choice category, and at grocery stores and wholesale clubs, then earn unlimited 1% thereafter. After the 3% first-year bonus offer ends, you will earn 3% and 2% cash back on these purchases up to the quarterly maximum.

- No annual fee and cash rewards don’t expire as long as your account remains open.

- Select your card design option when you apply – the Customized Cash Rewards design, or the limited-time FIFA World Cup 2026™ design.

- 0% Intro APR for 15 billing cycles for purchases, and for any balance transfers made in the first 60 days. After the Intro APR offer ends, a Variable APR that’s currently 17.49% – 27.49% will apply. A 3% Intro balance transfer fee will apply for the first 60 days your account is open. After the Intro balance transfer fee offer ends, the fee for future balance transfers is 5%. Balance transfers may not be used to pay any account provided by Bank of America.

- This offer may not be available elsewhere if you leave this page. You can take advantage of this offer when you apply now.

Additional Disclosure: Bank of America is a CardRates advertiser.

- Earn 20,000 bonus Points after spending $1,000 in the first 3 months of account opening.

- 0% Intro APR on balance transfers and purchases for 15 months; after that, the variable APR will be 18.49% – 28.49%, based on your creditworthiness. There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

- Earn 3 ThankYou® Points for each $1 spent in an eligible Self-Select Category of your choice (Fitness Clubs, Select Streaming Services, Live Entertainment, Cosmetic Stores/Barber Shops/Hair Salons, or Pet Supply Stores). Choose your eligible Self-Select Category on Citi Online or by calling customer service. The default Self-Select Category is Select Streaming Services.

- Earn 5 ThankYou® Points for each $1 spent on Hotels, Car Rentals and Attractions booked on Citi Travel® via cititravel.com; earn 3 ThankYou Points for each $1 spent at Supermarkets, on Select Transit purchases, and at Gas & EV Charging Stations.

- Earn 2 ThankYou® Points for each $1 spent at Restaurants; earn 1 ThankYou® Point for each $1 spent on All Other Purchases.

- No Annual Fee

Additional Disclosure: Citi is a CardRates advertiser.

After reviewing your budget, you discover that you can pay $200 every month to the card. This means you’ll pay the balance off in 15 months without ever being charged interest.

2. You Have High-Interest Debt

If you’ve acquired high-interest credit card debt that is costing you big time, a 0% balance transfer card can come to the rescue.

For example, if your current credit card has a $5,000 balance but the APR is 28%, it will take you 28 months with a $250 payment – and $1,813 in interest fees – to pay the card off. But you would save a lot of money and time with a balance transfer card.

But if you take advantage of a balance transfer card with a 0% APR, you will save over $1,000 in interest if you pay your balance off before the 0% promotion expires, even after you factor in a 5% balance transfer fee. Balance transfer fees generally range from 2% to 5% of the amount transferred.

3. You Want to Give Your Credit Score a Boost

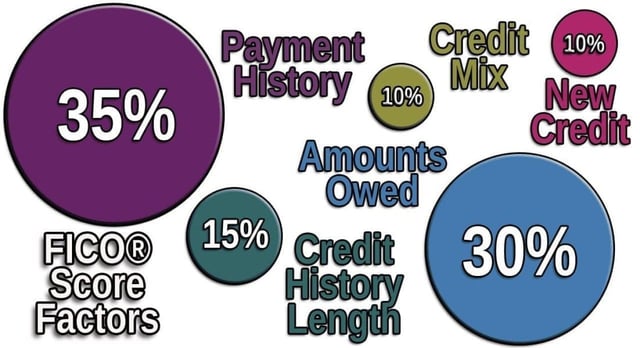

One of the problems of carrying a lot of credit card debt is that it can negatively affect your credit scores. Credit utilization is the second most important factor in a FICO Score, so if your card’s balance is close to the credit limit, it could be shaving points from your credit scores.

A balance transfer card can also be beneficial, assuming your credit scores are high enough to qualify. When you move your existing debt to the new card, the amount you owe on the original account will be at zero.

So not only will you benefit from the 0% APR, but you are also decreasing your credit utilization ratio, which can boost your credit score.

4. You Want to Buy Something Expensive

Of course, there are some occasions when you simply want to purchase an item or service that will cost you a lot of money. Instead of depleting the cash in your bank account, you can turn to a 0% APR card and leave your savings intact.

Perhaps you have your eye on a top-of-the-line Italian espresso machine for your kitchen. The price: $1,300. If you charged the machine to your existing credit card with a 24% APR and made $144 payments, it would take you 11 months to pay off — plus $148 in interest.

But if you opened a new credit card with 0% APR with the same $144 monthly payments, you would be out of debt in nine months — and you can spend the money you would have paid in interest on some super special coffee beans.

5. You Want to Score a Welcome Bonus

Maybe you want to enjoy an additional and immediate profit with a 0% APR credit card. The good news is that you probably can.

Some of these cards also come with welcome bonuses, including a fixed amount of cash or points when you open the card and spend enough in a certain period. Look around for a card that offers both benefits.

One such account is the Capital One Quicksilver Cash Rewards Credit Card. It has a 0% APR and will give you a cash bonus after you meet the spending minimum within the terms provided:

- Earn a one-time $200 cash bonus after you spend $500 on purchases within 3 months from account opening

- Earn unlimited 1.5% cash back on every purchase, every day

- $0 annual fee and no foreign transaction fees

- Earn unlimited 5% cash back on hotels, vacation rentals and rental cars booked through Capital One Travel

- No rotating categories or sign-ups needed to earn cash rewards; plus, cash back won’t expire for the life of the account and there’s no limit to how much you can earn

- 0% intro APR on purchases and balance transfers for 15 months; 18.49% – 28.49% variable APR after that; balance transfer fee applies

- Top rated mobile app

So not only will you get a substantial amount of time to make interest-free purchases, but you can score a couple of hundred dollars in the process.

6. You’re Also Interested in Accumulating Ongoing Rewards

The majority of these 0% APR cards also come with rewards programs with which you can earn miles, cash, or points when you make your charges. You’ll earn them during the 0% introductory period and for as long as your account is open and in good standing.

The key is to find the card that gives you the interest-free period you want, plus the right rewards program for your lifestyle.

For example, maybe you’ve been itching to get away. The Bank of America® Travel Rewards credit card comes with a 0% APR for purchases, a signup bonus, and point rewards. That means you can charge the price of a trip, have over a year to pay it off with no financing fees adding to the cost, and walk away with a cash bonus.

Qualifying For a 0% APR Card

Credit cards equipped with 0% APR deals are generally only available to applicants who have good to excellent credit. Check your credit scores before applying. These scores range from 300 to 850, with higher numbers preferable to lenders.

Good credit scores begin at around 670, so if yours falls short and you want to take advantage of one of these products, take action.

Because payment history is the most important credit scoring factor, make certain that you get all of your payments in on time for every account on your credit report.

If a high credit utilization ratio is holding your scores back and you can’t get a 0% balance transfer deal, pay some of the balance down first or ask your existing credit card issuer to give you a higher credit limit. This will increase your available credit line and lower your credit utilization ratio.

Check your credit reports to find out if they contain any errors that are lowering your credit scores. Dispute any errors you find immediately. Once they’re removed from your reports, your scores may rise enough for you to qualify for the card you want.

Consider enrolling in Experian Boost, which is offered by the credit bureau Experian. It’s a free program that allows you to add recurring payments, such as utility and cellphone bills, to your credit report. Your Experian FICO Score may rise when those timely payments are recorded.

Manage Your 0% APR Card Wisely

Once you have your 0% APR card, you can get the most out of the deal by managing the account responsibly.

First, it is crucial to pay off the debt within the defined time frame. Mark your calendar for when you need to make your final payment. If you keep a balance after that date, the purchase APR will go into effect. Keep constant watch of your account and send enough to be debt-free before the deal expires.

Also, make all of your payments on time and send no less than the minimum requested payment. Most of these offers are only good when you honor the terms of the agreement. That means you have to get at least your minimum payment in before or by the due date since even one late payment can cause the 0% APR to end early.

If you find yourself in a financial pinch and can’t pay the full amount, adjust your budget so you can. The last thing you want is for a 0% APR to zoom up to 20% or more when you can least afford the extra financing fees.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![10 Great Reasons to Consider a Travel Card[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2021/05/Reasons-to-Consider-a-Travel-Card.jpg?width=158&height=120&fit=crop "10 Great Reasons to Consider a Travel Card[updated_month_year before=\" (\" after=\")\"]")

![What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/05/what-is-apr.jpg?width=158&height=120&fit=crop "What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=\" (\" after=\")\"]")

![What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/11/good-apr2.png?width=158&height=120&fit=crop "What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=\" (\" after=\")\"]")

![7 Best 0% APR & Low-Interest Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2018/04/low.png?width=158&height=120&fit=crop "7 Best 0% APR & Low-Interest Credit Cards[updated_month_year before=\" (\" after=\")\"]")

![7 Longest 0% APR Credit Card Offers[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2019/11/Longest-0-APR-Credit-Card-Offers-Feat.png?width=158&height=120&fit=crop "7 Longest 0% APR Credit Card Offers[updated_month_year before=\" (\" after=\")\"]")

![7 Best Purchase APR Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2019/11/Best-Purchase-APR-Credit-Cards-Feat.jpg?width=158&height=120&fit=crop "7 Best Purchase APR Credit Cards[updated_month_year before=\" (\" after=\")\"]")

![9 Best High-Limit 0% APR Credit Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2023/03/Best-High-Limit-0-APR-Credit-Cards.jpg?width=158&height=120&fit=crop "9 Best High-Limit 0% APR Credit Cards[updated_month_year before=\" (\" after=\")\"]")

![Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2022/06/Can-I-Use-My-Credit-Card-Before-Closing-on-a-Home.jpg?width=158&height=120&fit=crop "Can I Use Credit Cards Before Closing on a Home?[updated_month_year before=\" (\" after=\")\"]")