Writer: Eric Bank

Editor: Austin Lang

Reviewer: Jon McDonald

Opinions expressed here are ours alone, and are not provided, endorsed, or approved by any issuer. Our articles follow strict editorial guidelines and are updated regularly.

Some of my friends love trading high-flying growth stocks, while my other friends safeguard their money in bank CDs. My risk-taking friends see volatility as their ally and have no qualms about owning variable APR credit cards, which can frequently change rates. To my play-it-safe friends, unpredictability is a nightmare, so it’s little surprise they prefer credit cards with fixed APRs.

A variable APR (Annual Percentage Rate) is a credit card interest rate that changes in response to the movements of a benchmark interest rate, typically the prime rate.

Keep reading to understand everything about variable APRs — from how they work to why some people prefer them.

-

Navigate This Article:

How APRs Work

Understanding how APR works is like knowing the rules of poker before you ante up. It means wrapping your head around exactly how much you are going to pay when you carry a balance on a credit card. Decoding the APR enigma enables you to make better choices in the showdown between you and your credit card issuer.

Interest Rates and APR

APR is an interest rate that approximates the annual cost of borrowing money from your credit card. You can use it to represent how much you’ll have to shell out for the year if you trigger credit card interest. Think of it as the price tag on the things you borrow, expressed as an annual rate.

Strictly speaking, an interest rate is the percent you owe for money loaned to you, whereas APR is the same thing expressed as a yearly rate. In the case of credit cards, folks pretty much use the terms interchangeably.

“An interest rate is the percent you owe for money loaned to you, whereas APR is the same thing expressed as a yearly rate. In the case of credit cards, folks pretty much use the terms interchangeably.”

APR is a little imprecise, as it doesn’t figure in fees or compounding — just the simple interest rate that you will cough up if you borrow from the card.

Just about all credit cards compound interest daily, which means a higher yearly price tag. Effective Annual Rate (EAR) is an APR that includes the effect of compounding.

Another shortcoming of APR is that it ignores credit card fees, even though you don’t have that luxury. APR isn’t aware of annual, late payment, signup, and maintenance fees. The lesson is that you can’t rely on APR alone to evaluate a credit card’s cost.

Fixed vs. Variable APRs

Now we’re down to the nitty gritty — let’s see exactly how variable APR stacks up against fixed APR.

Fixed APR is basically like being able to lock in the price of your favorite tall iced latte. You want the price to remain the same amount (exorbitant as it is) every time you pull up to the drive-through window.

Rain or shine, the price is secure. It’s funny — some folks are OK paying $6 for a cup of joe but complain bitterly if the cost rises to $6.50.

One hitch: You don’t want to get too comfortable with fixed APRs. Although they don’t go up and down with the market, they absolutely can change under special circumstances.

These circumstances include missing a payment or significant economic distress. The silver lining? The issuer has to give you a heads-up before making any changes, so you’ll have a little time to prepare (and maybe look around for a different credit card).

A fixed APR is constant, predictable, and perfect for planning a budget. On the other hand, a variable APR behaves like a roller coaster — moving in one direction and then the other — based on the market.

Fixed APRs will keep interest in check and make your life easier, while variable APRs may save you money when the prime rate is low but cost you more when it is high.

Key Differences

A fixed APR is blessedly boring, unlike a variable APR with its ever-changing, fickle finger of fate. Let’s take a closer look at how they differ:

- Rate Stability: A fixed APR keeps its interest rate stable, meaning you’ll face consistent charges. However, a variable APR can increase or decrease with the market, resulting in higher or lower interest rates and payments.

- Advance Notice for Changes: Both types must inform you in advance of any upcoming changes. Naturally, this pertains mostly to variable APRs, which can change frequently.

- Predictability: Fixed APRs mean your payments remain consistent, so budgeting is easier. Changes to variable APRs are about as predictable as the weather — you may be able to forecast the wind’s direction but have little luck nailing down its speed.

- Typical Availability: Fixed APRs are rare for credit cards nowadays. You see them on loans, but credit cards usually adopt variable APRs.

- Suitability: Fixed APRs are best for you if you hate surprises. Variable APRs suit folks who can manage changes, and they can be attractive to gamblers who hope to benefit if interest rates fall.

Some variable APR cards out there try to seduce you with a ridiculously low introductory interest rate, then slam you with a high rate later on. If you see a card advertising a laughably low variable APR, I would just ignore it — something hinky may be going on.

For example, I know of one credit card with a 9.99% APR! The catch is that it lacks a grace period, so your purchases accrue interest starting on day one.

How Variable APRs are Determined

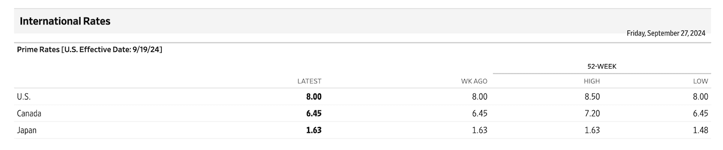

Variable APRs on credit cards move in accordance with the prime rate, the most commonly used base rate. When the prime rises, so does your APR, usually without any delay.

A fall in the prime rate will eventually cause APRs to decline, but it may take a little while. It seems that variable APRs are well-oiled on the upside but sticky on the downside.

“Your initial APR hinges on your credit score. With a strong score, you’re definitely in line for a better starting variable APR.”

In this sense, variable APRs work like gas prices. A sudden mismatch between gasoline demand and supply can send prices up a dollar or more, burning a hole in your budget. When supply becomes plentiful, gas prices will fall, but usually at a leisurely pace.

Many credit cards offer a range of APRs. Your initial APR hinges on your credit score. With a strong score, you’re definitely in line for a better starting variable APR. If your credit history is a little bumpy, expect your variable APR to start at the higher end of the credit card’s rate range.

Factors that Influence Variable APRs

Knowing what makes your credit card’s APR tick is as important as knowing when to take your favorite pie out of the oven. It can mean the difference between the sweetness of low costs and being burnt as costs soar.

Economic Changes

Think of the prime rate as the tide, lifting or lowering your credit card’s APR. As the prime rate rises, your variable APR typically moves right along with it — meaning you have to pay more interest when you carry a balance.

When the prime rate drops, your credit card will eventually (dare I say, reluctantly?) reduce your variable APR.

Remember that prime rate changes do not happen overnight and are fueled by the economy. Staying aware of economic trends can help you anticipate where interest rates are going.

Think of the Federal Reserve as the captain at the helm of the economic ship. Its decisions directly affect the financial system and interest rates. In particular, the Fed’s star chamber of regional directors periodically convenes to set the Fed Funds rate, the interest rate it charges to the biggest banks.

These decisions, in turn, affect the prime rate — what banks charge their best customers. If the economy is overheated, the Fed will raise its interest rate to cool things off. The dominoes then fall throughout the economy and land on your credit card.

If you’re carrying a credit card balance, changes in Federal Reserve policies and the prime rate can hit you where it counts: your wallet.

Staying informed about how the economic tides are turning can prepare you for APR changes. For example, a rate upsurge should motivate you to repay your balances.

Your Creditworthiness

A card’s intended audience speaks volumes about the lower and upper bounds of its variable APR range. As you’d expect, cards for fair or poor credit have higher APR ranges. Cards for the worst credit may have APRs fixed at 36%.

Even if you prefer a fixed APR, there’s little consolation from locking in an astronomical interest rate.

A good-to-excellent credit score buys you an address on Easy Street with an APR in the mid-to-upper teens. Whatever your score, it’s prudent to shop for a card that gives you the features you want most.

Here is a look at what you can expect to pay in credit card interest, depending on your credit score:

Your credit history shows lenders how responsible a borrower you’ve been. You can make this suspicious group less fearful by making on-time payments and carrying low balances. However, suppose your credit history is bruised, battered, and sore. In that case, lenders will pile on with higher interest rates and puny credit limits.

Talk about kicking a person when they’re down! Still, issuers are just as quick to celebrate your financial recovery with better rates, higher credit lines, and a bounty of benefits. They are truly your fair-weather friends.

Credit Card Terms and Conditions

I love reading cardmember agreements, don’t you? They contain stirring prose detailing your card’s terms and conditions — both the good stuff and the bad.

For example, those introductory 0% APR offers can be really tempting. But beware: That intro rate is temporary.

Your APR will jump up faster than a jackrabbit once the promotion period expires. That’ll leave you with hefty interest charges should you still owe money. I’d say that’s an excellent reason to pay off the balance before the promo ends.

If you pay off your balance before your card’s introductory promotion ends, you could sidestep a maountain of interest costs.

As important as it is to always pay your bills on time, it’s doubly critical during a 0% APR promotion period. That’s because a late payment will cause the issuer to remove the interest-free punch bowl and replace it with a sour concoction of late fees and a higher interest rate — either the card’s regular APR or its terrifying penalty APR, typically 29.9%.

It’s all there in the cardmember agreement’s tiny print. See why it makes such good reading?

Other gotchas hiding in your agreement may include a zero-day grace period so that you accrue interest right away. There’ll likely be all sorts of nuisance fees to trouble your sleep.

Cards for consumers with very poor credit are notorious for charging signup fees, 35.99% APRs, high annual fees, and even a monthly maintenance fee that can approach $100 yearly.

Here’s my nomination for the most abominable fee: Some cards take a piece of the action for any credit limit increases they dole out.

For example, they grab a $25 “gratuity” if they raise your credit limit from, say, $200 to $300. I’d like to think that Proverbs got it right: “The greedy bring ruin to their households.” But in the modern era, I’m not so sure — it’s more likely they bring ruin to your household.

Pros and Cons of Variable APRs

Variable APRs are a bit of a mixed bag. Certainly, they have advantages, but they also come with some drawbacks. Check out the rundown below to weigh the pros against the cons.

Advantages:

- Potential for lower rates when the prime rate is low: Your variable APR changes with the prime rate. If the prime rate drops, your APR will follow, meaning less interest will be generated on any carried balances. Every little bit helps. It’s like getting an unexpected (albeit tiny) discount when you’re checking out.

- Flexibility and potential cost savings for the cardholder: A variable-rate APR can save you money and allow you the flexibility to take advantage of lower interest rates. This is particularly valuable if you’ve been a good credit user.

Disadvantages:

- Unpredictability and potential for higher costs: As easily as a variable APR can go down, it can also go up. If the prime rate increases, so will your APR. It’s like playing craps — you never know if you’re going to make the point or seven out.

- Challenges in budgeting due to fluctuating rates: Your budget may become more difficult to manage if your card has a variable APR because the interest rate (which directly affects your payments when you carry a balance) can go up or down from month to month.

Variable APRs can be a good fit if you’re comfortable with some risk and are ready to take advantage of lower rates when they arrive. But if you treasure stability and predictability, you may want to think twice before signing up.

How to Manage Your Variable APR

A variable APR is much like riding a bucking bronco: You have to stay on top, or it will throw you for a loop. But here are a few simple tricks that can keep interest charges from galloping away with your hard-earned money.

Look For Interest Rate Changes

As I explained earlier, you need to watch interest rates, particularly the prime rate, as this is an almost certain guide for your variable APR. You can keep up with rate pressures through reputable sources. My favorite is The Economist (the best-written weekly journal, bar none).

The goal is to be prepared if and when rates change.

When following the economic news, pay attention if the Fed is about to announce a decision on interest rates. Its decisions can vault your APR almost immediately. It’s not a bad idea to set up financial alerts on your mobile device so you’ll stay on top of any changes.

You also need to check your credit card statements and any letters or emails that you get from your card company. Issuers must disclose APR changes in advance — typically 45 days before the new rates take effect.

Minimize Your Interest Costs

If you’re seeing interest rates move up, it’s a smart move to get rid of your unpaid balances. The less you owe, the less interest you’d be saddled with when your variable APR rises. Kind of like paying your tab before prices go up — better to settle now than to let the bill grow.

If you can’t pay your balance off all at once, consider getting a balance transfer card to shift your debt to a new credit card with an introductory 0% APR. Transfer fees typically range from 3% to 5%, but in return, you may save hundreds of dollars in interest.

Before you open a balance transfer card, make sure you know when that low APR will end and what the regular rate will be afterward. You want to avoid being caught by surprise when the honeymoon period is over.

Paying a few bucks more each month will repay the balance quicker and ultimately reduce your interest costs. Another trick is to divide your monthly payments into two and pay biweekly – it will lower your balance and interest costs more quickly.

Try to Negotiate With Credit Card Issuers

If you have a pretty good credit score and have been meeting your obligations, don’t hesitate to call your credit card company and ask it to reduce your APR. Sometimes, successfully getting a better deal is just a matter of asking.

When you call, make a compelling case for reducing your rate. Describe your on-time payments and your good credit history. Be polite but firm because you want to get your point across without ruffling any feathers. You certainly don’t want to end up with egg on your face.

If your APR has recently increased, maybe because you missed payments, explain how the inadvertent oversight was not because of money problems. Tell your credit card issuer what took place and how you have things under control again. Sound sincere — sometimes you have to fake it to make it.

If your credit card company won’t play ball, it may be time to find a new card with a lower APR. There are tons on offer so you may be able to hook another card easier than you think. When you have so many choices, you may not need to settle for less.

Monitor Rates if Your Credit Card Has a Variable APR

If your credit card has a variable APR, think of it like driving on a winding road: You’ve got to be alert to the twists and turns to avoid a financial fender bender. Keep your eyes peeled on interest rates to steer clear of nasty surprises.

It’s not about predicting the future with your crystal ball. It’s about being prepared when the road ahead takes a sudden turn.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/05/what-is-apr.jpg?width=158&height=120&fit=crop "What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=\" (\" after=\")\"]")

![What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/11/good-apr2.png?width=158&height=120&fit=crop "What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=\" (\" after=\")\"]")