Writer: Eric Bank

Editor: Austin Lang

Reviewer: Jon McDonald

Opinions expressed here are ours alone, and are not provided, endorsed, or approved by any issuer. Our articles follow strict editorial guidelines and are updated regularly.

Credit card APR is a term that is frequently used but not always understood. Sure, most folks have a notion that it’s some sort of interest rate, but what does it include, and what does it leave out? Does it truly represent what you’ll pay to use a credit card?

The annual percentage rate, or APR, is the standardized yearly rate credit card issuers charge when you carry a balance. It represents the cost of borrowing money and offers potential insight into how much interest you can expect to pay if you don’t keep up with your monthly payments.

The annual percentage rate (APR) tells you how much interest you will pay to carry a balance on your credit card over time, expressed as a yearly rate.

Paying interest isn’t fun, but I have some good news about APR: If you always pay off your monthly balance and avoid cash advances and regular balance transfers, you likely won’t pay a penny in interest — regardless of your card’s APR.

If you want to know more about how credit card APRs are calculated, what they include and exclude, the differences between fixed and variable APRs, and the many types of APRs, you’ve come to the right place.

-

Navigate This Article:

The Basics of Credit Card APRs

Understanding APR helps you know how credit card companies calculate it and the various forms it can take. If math leaves you with cold feet, skip the calculation section and continue to the Fixed vs. Variable APR section.

How Your APR is Calculated

APR represents the annualized cost of borrowing. The nominal APR refers to the simple one-year interest rate you’ll have to pay without considering compounding (i.e., paying interest on interest). The effective APR reflects the effect of compounding interest. Credit card ads typically quote nominal APRs.

For example, a credit card may advertise a nominal APR of 15%, but that rate ignores compounding interest from previous billing cycles. The effective APR takes compounding into account and usually winds up slightly higher.

Knowing the difference between these two may help you better estimate how much it will cost you to borrow. In the fine print of most credit card agreements, effective APR is spelled out so you can get a reasonable estimate of the total amount of interest you might end up paying yearly.

Effective APR is important when comparing credit cards that have different compounding schedules, although most cards nowadays use daily compounding.

Credit card issuers calculate APR each day using the daily periodic rate (DPR), which is the APR divided by 365 days. For example, if your credit card charged 18% interest annually, the daily periodic rate would equal 0.0493% (18% divided by 365). Each day, the interest charged is calculated by multiplying the DPR by the average daily balance to which interest applies.

When you compound the interest daily like this, you can end up owing a lot of extra money in just a single month. That’s why it’s best to pay off your outstanding balance ASAP before interest charges start to pile up.

Fixed vs. Variable APRs

A fixed APR can help you plan monthly payments more efficiently. This type of APR does not change because of market trends. However, issuers may change fixed APRs under certain specific conditions, such as if you make late payments.

A variable APR, on the other hand, fluctuates according to an underlying interest rate called the prime rate. This is usually the interest rate banks charge their most creditworthy customers, like the VIP rate for borrowing money.

Variable APRs are directly affected by changes to the prime rate and reflect changes in the general economic climate. Consider, for instance, the situation where interest rates rise due to action taken by the federal government. In this case, the increase in variable APRs would likely reflect the higher prime rate.

For example, suppose the Federal Reserve raises the interest rates it charges big banks (i.e., the federal funds rate) to help curb inflation. The effect would likely be that the prime rate would go up, as would credit card variable APRs. Most credit cards have variable APRs, so your interest payments could fluctuate with the economy.

A cushion is an amount a credit card issuer adds to the prime rate to determine a card’s variable APR. You might hear people refer to the cushion as the margin instead: it means the same thing either way. Your credit issuer will likely take your risk into account before setting the cushion.

For example, if the prime rate were 5% and the issuer tacked on a 15% cushion, its credit card’s variable APR would be 20%. This cushion is the extra amount the issuer charges to cover its costs and make a profit.

The cushion helps pay the issuer’s operating costs, accounts for cardmembers who don’t pay their bills, and provides the issuer with a handsome profit. Cushion percentages differ from one issuer to another and may even vary among credit cards from the same issuer.

When the prime rate decreases, so should your credit card’s variable APR. However, credit card APRs are slow to follow reductions in the prime rate. For some reason, credit card companies seem reluctant to pass on the savings to their customers.

Even if the prime rate drops significantly, your APR may decrease by much less or stay the same for a long time. That means monitoring your APR and looking for ways to reduce it, such as transferring balances to cards with better terms, is a good idea.

Other Types of APRs

Credit cards have different types of APRs, and each applies to a specific situation. The following list will help you understand how a credit card can charge interest.

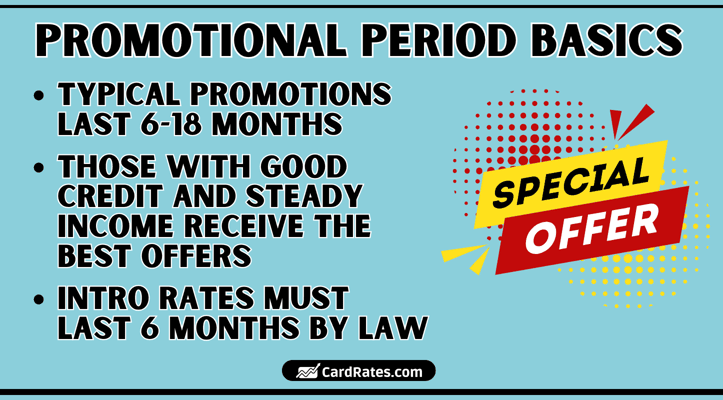

- Purchase APR: This APR applies to regular purchases from your credit card. This is the regular interest rate charged if you carry an unpaid balance month after month. The APR usually only applies if you don’t pay your balance before each month’s due date. The typical range is 11% to 36%. However, a card may offer new cardmembers a 0% purchase APR (typically for six to 18 months).

- Promotional Balance Transfer APR: You usually transfer a balance from one credit card to another during an introductory promotional period. This APR is typically 0% to entice new customers. It usually lasts six to 18 months, after which the regular balance transfer APR (generally equal to the purchase APR) commences.

- Cash Advance APR: This APR applies when you withdraw from an ATM or bank using your credit card. Usually higher than the purchase APR, this APR starts accruing interest immediately. Most cash advances impose a transaction fee, typically 3% to 5%. This APR usually ranges from 22% to 29% but could reach 36%.

- Penalty APR: This applies when you’ve violated the terms of your credit card agreement — for example, by not making a payment or exceeding the credit limit. The penalty APR is significantly higher than the regular purchase APR and can potentially remain in force indefinitely. The typical value is 29.9%, though there are many credit cards that do not charge a penalty APR.

Knowing these APRs and when they apply to your account will help you decide how to use your credit card. Comparing different cards to each other and to other lending sources can potentially save you some money on interest charges.

Factors that Influence Your Credit Card’s APR

Many factors contribute to the APR a card issuer may offer you. Understanding these factors can help you take action to lower the APR for which you may qualify.

Credit Score and History

Your credit score is one critical factor that most lenders use in determining your creditworthiness. A higher credit score indicates lower risk, making it more likely for issuers to offer you a lower APR.

On the other hand, a low credit score means elevated risk; therefore, you’ll likely receive high APR offers. Lenders use your credit history and score to predict the likelihood that you’ll repay your credit card debt.

Improving a low credit score can make you eligible for cards with lower APRs. Key tactics to build your score include paying bills on time, reducing debt, and not applying for new credit cards too often. I recommend you wait six months between applications.

A better credit score not only helps with lower APRs but also with better overall credit terms. You can monitor your credit reports regularly to identify areas that need improvement.

Current Economic Conditions

Economic conditions can play a massive role in determining credit card APRs. As explained earlier, variable APRs can increase when the prime rate goes up, usually due to higher inflation rates. Inflation also makes borrowing more expensive because lenders tend to adjust APRs to ensure they make an adequate after-inflation profit.

The state of the economy, especially the prime rate, influences whether you pay a low or high APR on your credit card.

The economy’s overall condition influences the available credit and interest rates in the marketplace. A sluggish economy usually encourages issuers to reduce APRs to stimulate demand for their cards.

Periods of economic expansion see APRs rise as borrowers compete for new credit. It’s wise to stay informed of economic trends to anticipate changes in your credit card APR.

How Your APR Impacts Debt and Borrowing Power

APR significantly impacts the interest you will pay over time on your credit card balance. The cost of carrying a balance is the total interest accumulated on your revolving credit if you fail to pay off your credit card balance every month. It’s essential to understand how APR impacts your costs when you owe money to your credit card.

Increases the Cost of Carrying a Balance

APR increases the expense of carrying a balance, making the debt costly. The higher your APR, the more interest you pay to carry an outstanding balance. With a high APR, more of your monthly payment goes to interest and less to your principal balance.

This will extend the time it takes to pay off your debt and increase your total interest cost — factors impacting your budget and ability to borrow.

Impact on Minimum Payments

A high APR can also influence your minimum payments. More of your payment goes to interest, meaning you have less money to pay off the principal. This can lead to a cycle of debt where you continuously accrue interest without significantly lowering your balance.

Higher APRs could mean higher minimum monthly payments, with a large portion of that going to interest instead of principal.

Making only minimum payments on high-APR cards can drag out your debt for very long periods and cost you more in interest. Make sure to understand how your APR affects debts so you can plan to pay down those balances effectively and, in doing so, lessen the cost of carrying credit card debt.

How to Compare Credit Cards With APRs in Mind

Comparing credit card APRs can save you money on interest charges. It’s essential to consider the different APRs offered and to use available resources to make a wise choice. Here are tips on how to effectively compare credit card APRs.

Carefully Evaluate Offers and Terms

Look at several different credit card offers and compare the standard purchase APRs, balance transfer APRs, and cash advance APRs. Estimate your total cost of carrying a balance and how the APR will affect your interest cost over time.

Introductory APR offers can be tempting, but the devil is in the details. Typically, these offers give you a much lower APR for a limited time and then start charging the regular APR. You need to know when an introductory period expires and the regular APR kicks in so you can avoid paying interest on unpaid balances.

Identify Promotional APRs and End Dates

One of the best uses of promotional APR offers is to pay down debt on other cards. Promotional 0% APRs for balance transfers or new purchases can eliminate your interest during the promotional period. They apply only to new cardmembers and generally expire six to 18 months after account opening.

Knowing the benefits and traps of promotional APRs helps maximize their value. Several snares can be hidden within APR promotions, so you must be cautious. One of those gotchas occurs when you don’t repay your entire balance within the promotion period. You must pay the card’s regular APR on any unpaid balance.

Some promotional deals state that you lose your right to the 0% APR if you miss a payment. That can really screw up your plans, so take care to always pay at least the minimum amount due on time.

Also, be aware that some balance transfer promotions require you to initiate transfers within a short deadline (e.g., 45 or 60 days after account opening) to qualify for the promotional APR.

Use Online Tools and Resources

Calculators and online tools can help you compare APRs. These calculators allow you to enter various credit card offers and compare APRs, fees, and other terms side-by-side.

Today, numerous online resources help you search for the best credit card offers with competitive APRs. Credit card comparison websites (such as CardRates.com), consumer finance blogs, and financial institution websites contain the best details and reviews. You can use these resources to determine your best credit card options and lock in a low APR.

Knowing Your Credit Card APRs Can Save You Money

You are ahead of the game when you understand the different types of credit card APRs and how they influence your budget. If you know the purchase, promotional, cash advance, and penalty APRs, you can make informed decisions when choosing and using a credit card.

This knowledge helps you avoid interest charges and manage debt more effectively. This will save money in the long run. Understanding what factors impact your APR, such as your credit score and current economic conditions, will help you take steps today to ensure lower interest rates.

It’s wise to shop for low credit card APRs if you plan to carry balances. Look around for the best deals, understand the terms governing the introductory and promotional APRs, and use online tools and resources to find credit card deals. Take your time researching and comparing credit cards that fit your financial requirements so you can keep interest costs to a minimum.

Editorial Note: Our site content is not provided or commissioned by any credit card issuer(s). Opinions expressed on CardRates.com are the author's alone, not those of any credit card issuer, and have not been reviewed, approved, or otherwise endorsed by credit card issuers. Every reasonable effort has been made to maintain accurate information; however, all credit card offer details, including information about rewards, signup bonuses, introductory offers, and other terms and conditions, is presented without warranty. Clicking on any offer on CardRates.com will direct you to the issuer's website, where you can review the current terms and conditions of the offer.

About the Author

![How to Calculate APR on a Credit Card[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2015/11/CalculateAPR-1--1.png?width=158&height=120&fit=crop "How to Calculate APR on a Credit Card[updated_month_year before=\" (\" after=\")\"]")

![How to Calculate Credit Card Interest: 3 Steps to Find Your Rate[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/02/how-to-calculate-credit-card-interest.jpg?width=158&height=120&fit=crop "How to Calculate Credit Card Interest: 3 Steps to Find Your Rate[updated_month_year before=\" (\" after=\")\"]")

![What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/11/good-apr2.png?width=158&height=120&fit=crop "What is a Good Credit Card APR? 5 Best Low APR Cards[updated_month_year before=\" (\" after=\")\"]")

![What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2017/05/what-is-apr.jpg?width=158&height=120&fit=crop "What is Credit Card APR? 9 Best 0% APR Cards[updated_month_year before=\" (\" after=\")\"]")

![7 Best Credit Card Interest Rates[updated_month_year before=" (" after=")"]](https://www.cardrates.com/images/uploads/2021/05/Best-Credit-Card-Interest-Rates.jpg?width=158&height=120&fit=crop "7 Best Credit Card Interest Rates[updated_month_year before=\" (\" after=\")\"]")