Eric Bank is an M.B.A. who has covered financial and business topics since 1985, appearing regularly on Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences, particularly in the world of personal finance. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.

Jon leverages 15-plus years of journalism expertise to inform financial consumers about emerging trends and companies making an impact in the industry. He is most knowledgeable in the areas of budgeting, credit card rewards, and responsible credit use. Jon has a passion for writing and editing, and his articles have appeared in publications produced by The New York Times.

For nearly 20 years, Andrew has worked for financial institutions ranging from regional investment organizations to some of the largest banks in the world. At Wells Fargo, Andrew was a Consultant within the Insight and Innovation division. A graduate of the University of Georgia’s Terry College of Business, Andrew’s goal has been promoting personal financial wellness and solid money decisions.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our Rating

Current Visa Debit

4.0/5.0

About this rating

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Online-only banks, which operate without brick-and-mortar branches, are popular due to their convenience and lower fees. These banks offer many of the same features as their traditional counterparts, including mobile deposits, debit and credit cards, online transfers, and real-time notifications directly, all through their apps.

Below, I review Current, a mobile banking app and debit card that provides a wide range of features for spending, saving, and investing. I’ll also examine some of its top competitors that contend for consumers willing to forsake bank branches for the speed and convenience of digital banking.

Current automatically issues the Current Visa Debit when you open an online account. You can use the card to spend the money you deposit in your account.

Current is a financial technology company, not a bank. Choice Financial Group, Member FDIC, and Cross River Bank, Member FDIC, provide banking services.

The account requires no credit checks or annual fees.

You can get paid up to two days faster with direct deposit and earn rewards on purchases.

Current checks all the boxes an online banking app should. I like its broad range of features, purchase rewards, and availability to consumers with no, limited, or bad credit. On the downside, the $3.50 charge for each cash deposit seems high, although it does provide alternative ways to add cash fee-free.

How to Qualify & Apply For the Card

You can apply for this mobile banking service by providing your phone number online and then downloading the Current App. It takes only a couple of minutes to open an account through the Current App.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more information, see our ad disclosure and review policy.

Advertiser Disclosure

CardRates.com is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free, we receive compensation for referrals for many of the offers listed on the site. Along with key review factors, this compensation may impact how and where products appear across CardRates.com (including, for example, the order in which they appear). CardRates.com does not include the entire universe of available offers. Editorial opinions expressed on the site are strictly our own and are not provided, endorsed, or approved by advertisers.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Earn points on swipes: Earn up to 7x the points on card swipes at over 14,000 participating merchants, then redeem them for cash back in your account.*

Get paid up to 2 days faster with direct deposit*

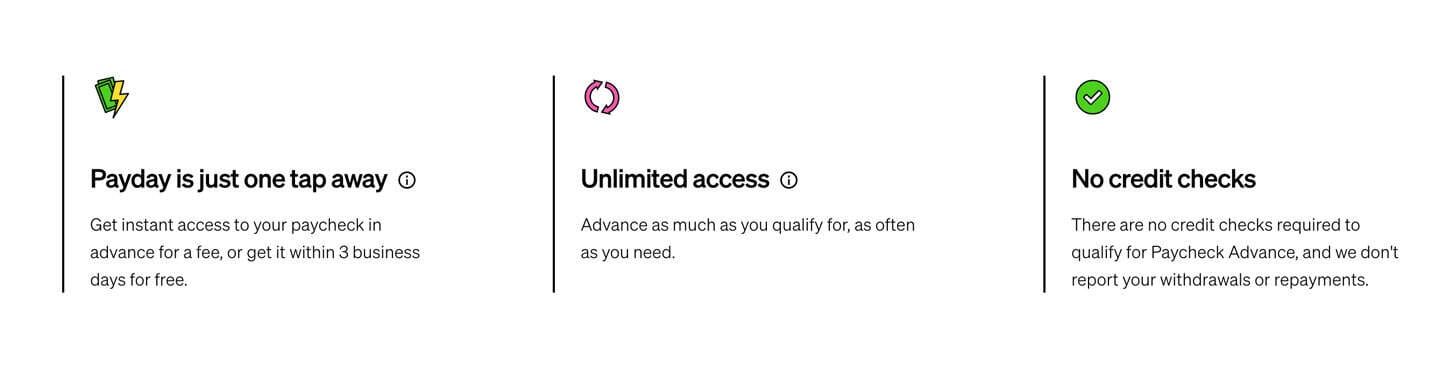

If you qualify, you can access up to $750 before payday with a paycheck advance

Qualifying direct deposits receive fee-free overdrafts*

No minimum balance fees, no overdraft fees, no bank transfer fees

The Current Account is available to US citizens and legal residents, 18 or older, with a valid Social Security number, mobile device, and email address. A parent can open a teen account for children under 18 years of age.

When you open an account, Current will send you its Visa debit card. You can also access and use the card virtually before the physical card arrives. Once you deposit cash into the account, you can immediately shop online and load the virtual card number into a digital wallet for in-person purchases.

The physical debit card should arrive within 10 days. Activate the card when it comes to using the mobile app and create a 4-digit security Personal Identification Number (PIN) for secure payments.

Benefits & Drawbacks to Consider

Understanding the benefits and drawbacks of a mobile banking app like Current can help you decide if it suits your financial needs. It can also help you compare Current to the competition and anticipate any service limitations so you’re ready for any surprises.

Benefits

No monthly fees: Current does not charge monthly fees.

Easy acceptance: You can get the account without a credit check or banking history.

Early direct deposit: You can receive your paycheck up to two days earlier than you can with traditional banks.

Budgeting features: The app offers tools to help you manage spending and save money.

Parental controls: For teen accounts, parents can monitor transactions and set spending limits.

Rewards: You earn points on select purchases that you can redeem for cash back.

Savings Pods: Create interest-bearing individual Savings Pods within your account to set aside money for specific goals.

Secured credit card: Establish or improve your credit score with a secured credit card that reports to all three major credit bureaus.

Drawbacks

No physical branches: Current does not have any physical bank locations or check-writing capabilities, which can be a drawback for those who prefer in-person banking services.

No interest on deposits: Money held in Current accounts does not earn interest unless you allocate it to a Savings Pod (maximum $6,000).

Charge for in-person cash deposits: You must pay $3.50 each time you deposit cash at a retail location.

ATM limitations: Free ATM withdrawals are limited to specific networks; using an out-of-network ATM incurs a $2.50 fee.

Deposit restrictions: The account sets limits on how much cash you can deposit at once, and fees apply for in-person deposits.

Customer service: Some users report that customer service can be slow or less responsive, especially during high-demand periods.

Overdraft services: You must direct deposit at least $500 monthly to qualify for Overdrive overdraft protection of $25 to $200.

The drawbacks are standard for this type of account. Overall, I judge the pros to outweigh the cons by a wide margin.

Other Cards Worth a Look

The following competes with the Current Visa Debit. Check fees before applying, as some are more expensive than the Current Account.

Our experts rate credit card offers based on factors like rewards, APRs, signup bonuses, fees, and approval rates, with a focus on benefits that provide the best value. We also consider cardholder needs such as credit-building potential, issuer reputation, and customer service. Our ratings are unbiased, updated regularly, and not influenced by issuers.

Overdraft protection up to $300 with opt-in and eligible direct deposit*

No monthly fees with eligible direct deposit, otherwise $5 per month

Earn up to 7% cash back when you buy eGift Cards in the app

Get your pay up to 2 days early - Get your government benefits up to 4 days early.*

High-yield savings account, 4.50% APY paid quarterly on savings up to $5,000.*

*Terms and conditions apply. GO2bank™ cards are issued by Green Dot Bank, Member FDIC, pursuant to a license from Visa U.S.A., Inc. Visa is a registered trademark of Visa International Service Association. Overdraft fees may apply. Click Apply Now to learn more.

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APRN/A

Annual FeeN/A

Credit NeededAll Credit Types Considered

The GO2bank™ Account provides many of the same features as Current. You can avoid its $5 monthly fee if you receive at least one payroll or government benefit direct deposit in the previous monthly statement period.

NetSpend® Visa® Prepaid Card

This card is currently not available.

Best Overall Rating

★★★★★

N/A

OVERALL RATING

N/A

Intro (Purchases)N/A

Intro (Transfers)N/A

Regular APRN/A

Annual FeeN/A

Credit NeededN/A

The NetSpend® Visa® Prepaid Card features direct deposit, rewards, mobile check deposits, and all the features you’d expect from a debit card. The only knock on this account is that you don’t have the ability to complement your card with a secured card as you can with a Chime Account.

Both accounts offer online banking services, high-yield savings accounts, and extensive ATM access. Overall, the two accounts impose similar deposit and transfer fees, but they both charge a fee if you open the account at a retail store.

Cardholder Reviews on Reddit

Checking online customer reviews of a Current Account can give you a real-world look into how the app performs and what issues you may experience. Reviews often highlight aspects such as reliability and customer service. They also provide a wide range of opinions, which can help you determine if the account will suit your needs.

“Current’s perks include up to 15x cash back on purchases. That needs to be redeemed in the app, and then you get the cash back as soon as the payment is processed. They offer paycheck direct deposits two days early, something my local credit union charges a monthly fee to offer. Current also has a perk that immediately removes gas pump holds.”

“I’ve been with them for six months but am about to switch. They say you get up to $200 in overdraft, but I’ve only been approved for $25, even though I have over $2,000 in direct deposits per month since I joined. They also claim to get your paycheck to you two days in advance, but it is frequently late for me.”

“I haven’t had any issues or need to contact support. I have read some posts from others who were frustrated by a dispute they had filed. Fortunately, I haven’t had any such issues. Another advantage of Current is that, so far, the debit card hasn’t been flagged as a prepaid card. Chime has always had issues with things like rental cars, etc., because companies consider them prepaid accounts. I have had no similar issues with Current.”

FAQs: How Do I Manage Funds in My Current Account?

The whole point of opening a Current Account is to allow you to conveniently manage funds without dealing with a brick-and-mortar bank. You can accomplish all of your banking tasks through the Current mobile app — no tellers, waiting lines, or high bank fees. Let’s take a closer look at how you use the account.

Deposits

You can add cash to your Current Account at any of the retailers listed in the Current app, including CVS and Walmart. The cashier scans a barcode from the app, and you provide the cash to deposit. Current charges $3.50 for each cash deposit.

You can add up to $500 per transaction and up to $1,000 per day. In addition, you can add up to $10,000 per month in cash.

Alternatively, you can deposit checks via the Current mobile app. Start by entering the check amount and where you want the money to go. Before depositing your check, sign the back of it and write “Current/Mobile Check Deposit,” or Current may reject it. Then, snap photos of the endorsed check’s front and back.

Consumers can directly deposit their paychecks with Current’s mobile app.

The app will transmit the deposit for immediate processing. You cannot use the mobile check deposit feature to fund your account for the first time. You can deposit up to $2,000 per check, with a daily maximum of $2,000.

The app will transmit the deposit for immediate processing. You cannot use the mobile check deposit feature to fund your account for the first time. You can deposit up to $2,000 per check, with a daily maximum of $2,000.

You can transfer funds into your Current Account from any of your internal or external linked funding sources, including Savings Pods, Teen Accounts, cash advance apps, PayPal, and other banks. Current uses the Plaid platform to link external accounts. Most ACH withdrawals settle in one to three business days but can take up to five business days, depending on your bank. You can set up single and repeating transfers via the Current app.

Another way to add money to your Current Account is through an instant transfer from a third-party service. Some apps, including Venmo and Cash App, allow you to instantly cash out your balance to your debit card.

You can add your physical or virtual Current debit card to any service that accepts it, and transfers of your balance to the debit card should arrive almost instantly. This feature is not available for Teen Accounts.

You cannot deposit money via an ATM.

Spending

You can use the Current Visa Debit anywhere that accepts Visa® cards, including online merchants. You don’t pay any additional fees for using the card, except when traveling internationally. You can use the debit card to make purchases and pay bills up to your account balance. A $2,000 daily limit applies (although Current may allow transactions that exceed your limit).

Fee-free overdrafts are available to qualifying members. This privilege allows you to overdraw your account when you swipe your Current debit card and the feature comes at no additional cost. Current determines your eligibility for its Overdrive overdraft protection based on your direct deposit history, account activity, and other risk factors. To qualify, you must receive $500 or more in qualifying deposits over the preceding 30-day period.

Current cards are equipped to provide early access to your paychecks and overdraft protection.

Qualifying deposits for fee-free overdraft include ACH direct deposits from your employer, payroll provider, or government payroll. You’ll receive a notification from Current saying you’re eligible for fee-free overdrafts if your account qualifies. Once enabled, you can check your limit (from $25 to $200) on the mobile app.

Overdrafts create a negative balance in your Current Account. Current may restrict or close your account and terminate your access to the Overdrive feature if you don’t repay the negative balance within 60 days.

Withdrawals

The card allows you to withdraw cash at more than 40,000 Allpoint® ATMs across the country without any fees. To locate in-network ATMs, follow the steps in the Current app. You can withdraw up to $500 per day from ATMs.

You will face a charge if you withdraw cash from an out-of-network ATM. This comes in the form of a $2.50 domestic cash withdrawal fee separate from any fee the ATM operator may impose.

A merchant may allow you to get cash back at a point-of-sale location. You enter an amount greater than the purchase total, and the cashier will return the difference in cash. The limit for this type of withdrawal is $500 per day.

You can also go into any bank that accepts Visa® and request an over-the-counter (OTC) withdrawal. This method also has a $500 daily cap.

Transfers

As mentioned earlier, you can transfer money into your Current Account from a linked account. You can also transfer money out the same way, but the recipient must have an active Current Account.

This service is fee-free. You can send or receive up to a maximum of $2,500 per rolling 24-hour period.

Savings

You can create up to three Savings Pods within the mobile app. You earn 4% interest on your total savings, up to $6,000 per account. Opening a Savings Pod does not require a credit check, and no minimum balance is required.

To add funds to a Savings Pod, you can move money directly from your Current Account up to the available balance. You can also opt in to a feature that rounds up card purchases to the next dollar on each swipe purchase. Current transfers the difference to a Savings Pod when the transaction settles.

Is the Current Account Legitimate?

Current is a fintech company founded in 2018 and headquartered in New York City. The Better Business Bureau has not accredited Current but has given it an A- rating and customer reviews on the BBB give Current a middle-of-the-road rating.

Trustpilot gives Current an Excellent rating with around 70% of customers giving it five stars.

By all appearances, Current is a legitimate financial technology company. And Choice Financial Group, its partner bank, is FDIC-insured.

Can the Card Help My Credit Score?

The Current Visa Debit cannot directly impact your credit score because it doesn’t provide a credit line or report to the credit bureaus. However, Current offers a secured credit card, the Build Card, which can help establish or improve your credit score.

The Current Build card is a secured card designed to help users build their credit.

Unlike other secured credit cards, the Build Card allows you to add money to your Current Account to update your spending balance. You do not need to load money onto your Build Card separately.

By using the Build Card responsibly — including making purchases and paying off the balance on time — you can improve and build your credit history, as the card reports your activity to the three major credit bureaus.

What If Current Denies My Application?

Current is more likely to approve your application rather than deny it since it doesn’t perform credit checks. However, if it does reject your application, first make sure you are eligible and meet the residence, age, email, and Social Security number requirements.

Under the Fair Credit Reporting Act (FCRA), a bank using information from a consumer report to deny your application for a checking or savings account must provide you with an Adverse Action Notice.

You can also ask Current for an explanation of the specific reasons behind its decision. Current may reject your application if you owe fees to another bank. If you do, pay them promptly, preferably a few months before you apply to Current.

You can apply to accounts similar to Current, such as the one reviewed above. Alternatively, consider getting a reloadable prepaid debit card, which may provide some of the same features as a bank debit card but is much easier to get.

This Card May Be For You If…

You value having a debit card with no monthly fees and access to features such as early direct deposit and instant gas hold refunds.

You prefer banking entirely online and using mobile app features for budgeting, Savings Pods, and managing your finances on the go.

You are a parent looking for a teen account with robust parental controls to help manage and monitor your child’s spending habits effectively.

The Current Visa Debit stands out for its underlying Current Account, fee structure, and mobile banking features. It caters to tech-savvy users and families with teens through its powerful functionalities and parental control options.

However, Current lacks physical branches and check-writing capabilities, which may be dealbreakers for some. Before applying, check out the three alternative online banking apps I reviewed above.

About the Author

Eric Bank is an M.B.A. who has covered financial and business topics since 1985. He has contributed regularly to Credible, eHow, WiseBread, The Nest, Zacks, Chron, BadCredit.org, and dozens of other outlets. Eric specializes in taking complex subject matters and explaining them in simple terms for consumer audiences. Eric holds a Master's in Business Administration from New York University and a Master's in Finance from DePaul University.